Entry

Reader's guide

Entries A-Z

Subject index

Least Squares

The least squares method—a very popular technique—is used to compute estimations of parameters and to fit data. It is one of the oldest techniques of modern statistics, being first published in 1805 by the French mathematician Legendre in a now-classic memoir. But this method is even older because it turned out that, after the publication of Legendre’s memoir, Gauss, the famous German mathematician, published another memoir (in 1809) in which he mentioned that he had previously discovered this method and used it as early as 1795. A somewhat bitter anteriority dispute followed (a bit reminiscent of the Leibniz-Newton controversy about the invention of calculus), which, however, did not diminish the popularity of this technique. Galton used it (in 1886) in his work on the heritability of size, which laid down the foundations of CORRELATION and (also gave the name) REGRESSION analysis. Both Pearson and Fisher, who did so much in the early development of statistics, used and developed it in different contexts (FACTOR ANALYSIS FOR PEARSON AND EXPERIMENTAL DESIGN for Fisher).

Nowadays, the least squares method is widely used to find or estimate the numerical values of the parameters to fit a function to a set of data and to characterize the statistical properties of estimates. It exists with several variations: Its simpler version is called ORDINARY LEAST SQUARES (OLS); a more sophisticated version is called WEIGHTED LEAST SQUARES (WLS), which often performs better than OLS because it can modulate the importance of each observation in the final solution. Recent variations of the least squares method are alternating least squares (ALS) and PARTIAL LEAST SQUARES (PLS).

Functional FIT Example: Regression

The oldest (and still most frequent) use of OLS was LINEAR REGRESSION, which corresponds to the problem of finding a line (or curve) that best fits a set of data. In the standard formulation, a set of N pairs of observations {Yi, Xi} is used to find a function giving the value of the dependent variable (Y) from the values of an independent variable (X). With one variable and a linear function, the prediction is given by the following equation:

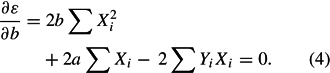

This equation involves two free parameters that specify the intercept (a) and the slope (b) of the regression line. The least squares method defines the estimate of these parameters as the values that minimize the sum of the squares (hence the name least squares) between the measurements and the model (i.e., the predicted values). This amounts to minimizing the following expression:

where ε stands for “error,” which is the quantity to be minimized. This is achieved using standard techniques from calculus—namely, the property that a quadratic (i.e., with a square) formula reaches its minimum value when its derivatives vanish. Taking the derivative of ε with respect to a and b and setting them to zero gives the following set of equations (called the normal equations):

and

Solving these two equations gives the least squares estimates of a and b as

with MY and MX denoting the means of X and Y, and

OLS can be extended to more than one independent variable (using matrix algebra) and to nonlinear functions.

...

- Analysis of Variance

- Association and Correlation

- Association

- Association Model

- Asymmetric Measures

- Biserial Correlation

- Canonical Correlation Analysis

- Correlation

- Correspondence Analysis

- Intraclass Correlation

- Multiple Correlation

- Part Correlation

- Partial Correlation

- Pearson's Correlation Coefficient

- Semipartial Correlation

- Simple Correlation (Regression)

- Spearman Correlation Coefficient

- Strength of Association

- Symmetric Measures

- Basic Qualitative Research

- Basic Statistics

- F Ratio

- N(n)

- t-Test

- X¯

- Y Variable

- z-Test

- Alternative Hypothesis

- Average

- Bar Graph

- Bell-Shaped Curve

- Bimodal

- Case

- Causal Modeling

- Cell

- Covariance

- Cumulative Frequency Polygon

- Data

- Dependent Variable

- Dispersion

- Exploratory Data Analysis

- Frequency Distribution

- Histogram

- Hypothesis

- Independent Variable

- Measures of Central Tendency

- Median

- Null Hypothesis

- Pie Chart

- Regression

- Standard Deviation

- Statistic

- Causal Modeling

- Discourse/Conversation Analysis

- Econometrics

- Epistemology

- Ethnography

- Evaluation

- Event History Analysis

- Experimental Design

- Factor Analysis and Related Techniques

- Feminist Methodology

- Generalized Linear Models

- Historical/Comparative

- Interviewing in Qualitative Research

- Latent Variable Model

- Life History/Biography

- Log-Linear Models (Categorical Dependent Variables)

- Longitudinal Analysis

- Mathematics and Formal Models

- Measurement Level

- Measurement Testing and Classification

- Multilevel Analysis

- Multiple Regression

- Qualitative Data Analysis

- Sampling in Qualitative Research

- Sampling in Surveys

- Scaling

- Significance Testing

- Simple Regression

- Survey Design

- Time Series

- ARIMA

- Box-Jenkins Modeling

- Cointegration

- Detrending

- Durbin-Watson Statistic

- Error Correction Models

- Forecasting

- Granger Causality

- Interrupted Time-Series Design

- Intervention Analysis

- Lag Structure

- Moving Average

- Periodicity

- Serial Correlation

- Spectral Analysis

- Time-Series Cross-Section (TSCS) Models

- Time-Series Data (Analysis/Design)

- Trend Analysis

- Loading...

Get a 30 day FREE TRIAL

-

Watch videos from a variety of sources bringing classroom topics to life

Watch videos from a variety of sources bringing classroom topics to life -

Read modern, diverse business cases

-

Explore hundreds of books and reference titles

Read next

More like this

Sage Recommends

We found other relevant content for you on other Sage platforms.

Have you created a personal profile? Login or create a profile so that you can save clips, playlists and searches