Entry

Reader's guide

Entries A-Z

Subject index

Heteroskedasticity

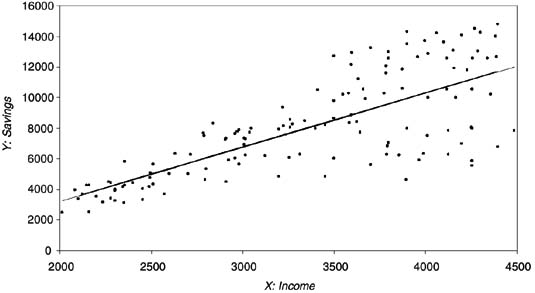

An assumption necessary to prove that the ORDINARY LEAST SQUARES (OLS) estimator is the BEST LINEAR UNBIASED ESTIMATOR (BLUE) is that the variance of the error is constant for all observations, or HOMOSKEDASTIC. Heteroskedasticity arises when this assumption is violated because the error variance is nonconstant. When this occurs, OLS parameter estimates will be unbiased, but the variances of the estimated parameters will not be efficient. A classic example is the regression of income on savings (Figure 1 provides a hypothetical visual example). We expect savings to increase as the level of income rises. This regression is heteroskedastic because individuals with low incomes have little money to save, and thus all have a relatively small amount of savings and small errors (they are all located near the regression line). However, individuals with high incomes have more to save, but some choose to use their surplus income in other ways (for instance, on leisure), so their level of savings varies more and the errors are larger.

Figure 1 Heteroskedastic Regression

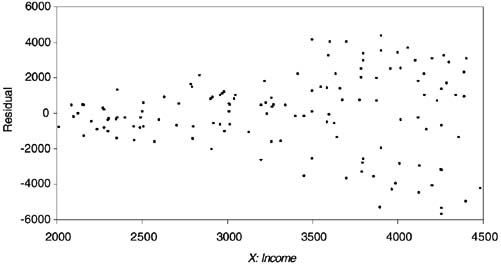

Figure 2 Visualizing Residuals

A number of methods to detect heteroskedasticity exist. The simplest is a visual inspection of the residuals Ûi = (yi −ŷi) plotted against each independent variable. If the absolute magnitudes of the residuals seem to be constant across values of all independent variables, heteroskedasticity is likely not a problem. If the dispersion of errors around the regression line changes across any independent variable (as Figure 2 shows it does in our hypothetical example), heteroskedasticity may be present. In any event, more formal tests for heteroskedasticity should be performed.

The Goldfeld-Quandt and Breusch-Pagan tests are among the options. In the former, the observations are ordered according to their magnitude on the offending variable, some central observations are omitted, and separate regressions are performed on the two remaining groups of observations. The ratio of their sum of squared residuals is then tested for heteroskedasticity. The latter test is more general, in that it does not require knowledge of the offending variable.

If the tests reveal the presence of heteroskedasticity, a useful first step is to again scrutinize the residuals to see if they suggest any omitted variables. It is possible that all over-predictions have a trait in common that could be controlled for in the model. In the example, a measure of the inherent value individuals place on saving money (or on leisure) could alleviate the problem. The high income-low savings individuals may value saving less (or leisure more) than the average individual. If no such change in model specification is apparent, it may be necessary to transform the variables and conduct a GENERALIZED LEAST SQUARES (GLS) estimation. The GLS procedure to correct for heteroskedasticity weights the observations on the offending independent variable by the inverse of their errors and is often referred to as WEIGHTED LEAST SQUARES (WLS). If the transformation is done, and no other regression assumptions are violated, transformed estimates are BLUE.

References

...

- Analysis of Variance

- Association and Correlation

- Association

- Association Model

- Asymmetric Measures

- Biserial Correlation

- Canonical Correlation Analysis

- Correlation

- Correspondence Analysis

- Intraclass Correlation

- Multiple Correlation

- Part Correlation

- Partial Correlation

- Pearson's Correlation Coefficient

- Semipartial Correlation

- Simple Correlation (Regression)

- Spearman Correlation Coefficient

- Strength of Association

- Symmetric Measures

- Basic Qualitative Research

- Basic Statistics

- F Ratio

- N(n)

- t-Test

- X¯

- Y Variable

- z-Test

- Alternative Hypothesis

- Average

- Bar Graph

- Bell-Shaped Curve

- Bimodal

- Case

- Causal Modeling

- Cell

- Covariance

- Cumulative Frequency Polygon

- Data

- Dependent Variable

- Dispersion

- Exploratory Data Analysis

- Frequency Distribution

- Histogram

- Hypothesis

- Independent Variable

- Measures of Central Tendency

- Median

- Null Hypothesis

- Pie Chart

- Regression

- Standard Deviation

- Statistic

- Causal Modeling

- Discourse/Conversation Analysis

- Econometrics

- Epistemology

- Ethnography

- Evaluation

- Event History Analysis

- Experimental Design

- Factor Analysis and Related Techniques

- Feminist Methodology

- Generalized Linear Models

- Historical/Comparative

- Interviewing in Qualitative Research

- Latent Variable Model

- Life History/Biography

- Log-Linear Models (Categorical Dependent Variables)

- Longitudinal Analysis

- Mathematics and Formal Models

- Measurement Level

- Measurement Testing and Classification

- Multilevel Analysis

- Multiple Regression

- Qualitative Data Analysis

- Sampling in Qualitative Research

- Sampling in Surveys

- Scaling

- Significance Testing

- Simple Regression

- Survey Design

- Time Series

- ARIMA

- Box-Jenkins Modeling

- Cointegration

- Detrending

- Durbin-Watson Statistic

- Error Correction Models

- Forecasting

- Granger Causality

- Interrupted Time-Series Design

- Intervention Analysis

- Lag Structure

- Moving Average

- Periodicity

- Serial Correlation

- Spectral Analysis

- Time-Series Cross-Section (TSCS) Models

- Time-Series Data (Analysis/Design)

- Trend Analysis

- Loading...

Get a 30 day FREE TRIAL

-

Watch videos from a variety of sources bringing classroom topics to life

Watch videos from a variety of sources bringing classroom topics to life -

Read modern, diverse business cases

-

Explore hundreds of books and reference titles

Read next

More like this

Sage Recommends

We found other relevant content for you on other Sage platforms.

Have you created a personal profile? Login or create a profile so that you can save clips, playlists and searches