Entry

Reader's guide

Entries A-Z

Subject index

Durbin-Watson Statistic

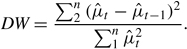

The Durbin-Watson (1950) statistic (DW or d) is a commonly used and routinely reported diagnostic test for the presence of first-order auto or serial correlation in the error of a time-series regression model. The statistic is calculated using the residuals from the regression we care about, μ^t as follows:

The null hypothesis for the test is that there is no first-order autocorrelation in the regression errors. The test has two alternatives: positive and negative first-order autocorrelation.

It is illustrative to express the test statistic directly in terms of the first-order autocorrelation ρ:

Written in this form, it is easy to see the relationship between the value of the test statistic and the degree of autocorrelation in the model residuals. Specifically, if there is no autocorrelation (ρ = 0), DW is approximately 2; if there is perfect positive autocorrelation (ρ = 1), DW is approximately 4; and if there is perfect negative autocorrelation (ρ = −1), DW is approximately 0.

The critical values for the test vary as a function of sample size and the degrees of freedom associated with the regression of interest. Typically, the DW test is computed for the alternative hypothesis of positive first-order autocorrelation so that we are looking for a value of DW that is significantly smaller than 2. Given difficulties in deriving the distribution of the DW statistic under the null hypothesis, two critical values are needed for each alternative hypothesis.

The test is appropriate only if there are no lagged dependent variables on the right-hand side of the regression we care about. If the regression contains a lagged dependent variable, alternative tests include Durbin's alternative, Durbin's H, or Lagrange multiplier tests. Similarly, DW will not detect higher orders of autocorrelation. To test for second and higher orders of autocorrelation in the errors, one can use Lagrange multiplier tests.

Finding a significant DW statistic indicates autocorrelation, which will invalidate hypothesis tests on the regression parameters we care about. A significant DW statistic is generally evidence of model misspecification, but may indicate that the errors are themselves serially correlated (Wooldridge, 2000). The appropriate remedial response varies based on the cause of the problem. The model may require that the right-hand side of the equation include a lagged dependent variable or other dynamic regressors. Alternatively, we may need to estimate the regression with feasible generalized least squares (GLS) by transforming the variables, reestimating the original regression to remove the autocorrelation, and estimating the resulting regression.

To illustrate, suppose we wish to model the voter turnout rate of women in the United States, (vt), from 1921 to the present, as a function of the mean level of education of women (et) and percent of women employed outside the home (wt). To test for first-order serial correlation, we would first save the residuals from the following regression model:

The residuals would then be used to compute the DW statistic as above. For a regression with a sample of size t = 45 and 3 degrees of freedom (two regressors plus a constant), the 5% critical values for the alternative of positive autocorrelation are 1.45 (lower) and 1.62 (upper). Assuming an estimated DW = 1.8, we could not reject the null hypothesis that there is no positive autocorrelation, and we would infer that there is probably no first-order autocorrelation. If the estimated DW = 1.4, we would reject the null hypothesis of no positive autocorrelation. For all values between 1.45 and 1.62, the test is inconclusive, and we would infer that there probably is first-order autocorrelation.

...

- Analysis of Variance

- Association and Correlation

- Association

- Association Model

- Asymmetric Measures

- Biserial Correlation

- Canonical Correlation Analysis

- Correlation

- Correspondence Analysis

- Intraclass Correlation

- Multiple Correlation

- Part Correlation

- Partial Correlation

- Pearson's Correlation Coefficient

- Semipartial Correlation

- Simple Correlation (Regression)

- Spearman Correlation Coefficient

- Strength of Association

- Symmetric Measures

- Basic Qualitative Research

- Basic Statistics

- F Ratio

- N(n)

- t-Test

- X¯

- Y Variable

- z-Test

- Alternative Hypothesis

- Average

- Bar Graph

- Bell-Shaped Curve

- Bimodal

- Case

- Causal Modeling

- Cell

- Covariance

- Cumulative Frequency Polygon

- Data

- Dependent Variable

- Dispersion

- Exploratory Data Analysis

- Frequency Distribution

- Histogram

- Hypothesis

- Independent Variable

- Measures of Central Tendency

- Median

- Null Hypothesis

- Pie Chart

- Regression

- Standard Deviation

- Statistic

- Causal Modeling

- Discourse/Conversation Analysis

- Econometrics

- Epistemology

- Ethnography

- Evaluation

- Event History Analysis

- Experimental Design

- Factor Analysis and Related Techniques

- Feminist Methodology

- Generalized Linear Models

- Historical/Comparative

- Interviewing in Qualitative Research

- Latent Variable Model

- Life History/Biography

- Log-Linear Models (Categorical Dependent Variables)

- Longitudinal Analysis

- Mathematics and Formal Models

- Measurement Level

- Measurement Testing and Classification

- Multilevel Analysis

- Multiple Regression

- Qualitative Data Analysis

- Sampling in Qualitative Research

- Sampling in Surveys

- Scaling

- Significance Testing

- Simple Regression

- Survey Design

- Time Series

- ARIMA

- Box-Jenkins Modeling

- Cointegration

- Detrending

- Durbin-Watson Statistic

- Error Correction Models

- Forecasting

- Granger Causality

- Interrupted Time-Series Design

- Intervention Analysis

- Lag Structure

- Moving Average

- Periodicity

- Serial Correlation

- Spectral Analysis

- Time-Series Cross-Section (TSCS) Models

- Time-Series Data (Analysis/Design)

- Trend Analysis

- Loading...

Get a 30 day FREE TRIAL

-

Watch videos from a variety of sources bringing classroom topics to life

Watch videos from a variety of sources bringing classroom topics to life -

Read modern, diverse business cases

-

Explore hundreds of books and reference titles

Read next

More like this

Sage Recommends

We found other relevant content for you on other Sage platforms.

Have you created a personal profile? Login or create a profile so that you can save clips, playlists and searches