Entry

Reader's guide

Entries A-Z

Subject index

Housing Demand

Housing stock and the associated housing services often constitute families’ biggest out-of-pocket spending expenses, and housing bundles often constitute their biggest and only savings instruments. Further, housing defines neighborhood quantity and quality and is often characterized in terms of desirable social outcomes.

Early Demand Analyses

Economists have long sought to identify determinants of housing demand. Unlike most economic goods, dwellings do not have easily identified units of service or easily identified prices for those services. As a result, analysts often concentrated on aggregate housing expenditures as fractions of income and on the impacts of changes in incomes and prices on these expenditures.

Richard Muth and Margaret Reid found that 1% increases in income were accompanied by substantial increases in housing expenditures. Economists standardize these measures as elasticities, with income elasticity as the following:

The matching 1% increases of income and expenditures imply constant income shares, or income elasticities, of about +1.0 (or in Reid's analyses, even higher).

Similarly, looking across groups of households, or countries with similar incomes, housing expenditure shares seemed to be about constant regardless of the prices. Similar to the income elasticity, the price elasticity is as follows:

In demand theory, constant shares imply a price elasticity of −1.0, where higher prices lead to an equal offset in quantity purchased.

Combining these estimates with emerging urban economic theory explained the incongruity of poor people living in central cities on high-priced land in high-priced housing, whereas more affluent people commuted farther as they demanded more and cheaper land (housing) in the suburbs. However, the aggregate analyses did not predict how individual families would react to changes in economic variables, such as price or income, or to changed demographic conditions, such as larger (or smaller) household size. The aggregate analyses did not address why some families rented and others owned, and they did not provide good guidance into how to implement demand-related housing policies.

Microlevel Analyses

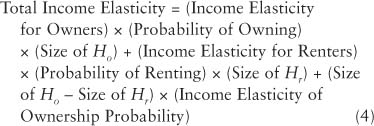

With improved data and computing methods, housing analysts focused on microeconomic and econometric analyses. Modern housing demand analysis starts with the identity that housing is either owned or rented and examines the behavioral determinants:

Analysts recognize that owner demand, renter demand, and probability of owning have behavioral components related to income (Y), owner or renter price (Po or P r), and demographics (D). An increase in income affects the quantities purchased by owners (H o), quantities purchased by renters (H r), and the decision of whether to own or rent (f). This income effect can be parsed into three parts:

The first two effects look at owner and renter demand separately, and the third recognizes that owner housing was traditionally “bigger” than renter housing and gave a bigger “bump” to housing demand. Similar decompositions apply to prices and demographic effects.

Measuring microlevel housing demand required advances in applied techniques. Neither income nor price is unambiguous. Because of the high transactions costs of moving, most analysts relate demand to permanent income, following Milton Friedman. Observed income Y is the sum of permanent Y P and transitory Y T income components, and econometric theory shows how permanent income can be estimated as the return to human and nonhuman capital. Appropriate decomposition often doubles estimated “observed income” elasticities.

...

- Abandonment

- Blight

- Displacement

- Eviction

- Filtering

- Not in My Back Yard (NIMBY)

- Obsolescence

- Substandard Housing

- Vacancy Rate

- Affordability

- Employer-Assisted Housing

- Extended-Stay Motels

- Fair Market Rent

- Foreclosures

- Housing Costs

- Housing Trust Funds

- Impact Fees

- Linkage

- Shared Group Housing

- Shelter Poverty

- Usury Laws

- Workforce Housing

- Behavioral Aspects

- Castle Doctrine

- Commuting

- Crime Prevention

- Crowding

- Cultural Aspects

- Feng Shui

- Home

- Housing Adjustment Theory

- Immigration and Housing

- Migration

- Mortgage Fraud

- Postoccupancy Evaluation

- Residential Autobiographies

- Residential Location

- Residential Mobility

- Residential Preferences

- Tenant Organizing in the United States, History of

- Cohousing

- Common Interest Development

- Community Development Block Grant

- Community Development Corporations

- Community Land Trust

- Community-Based Housing

- Company Housing

- Condominium

- Cooperative Housing

- Gated Community

- Homeowners’ Association

- Housing Counseling

- Land Bank

- Limited-Equity Cooperatives

- Military-Related Housing

- Mutual Housing

- Native Americans

- Neighborhood Stabilization Program

- Nonprofit Housing

- Participatory Design and Planning

- Planned Unit Development

- Pueblos

- Religion and Housing

- Resident Management

- Rural Housing

- Self-Help Housing

- Slaves, Housing of

- Social Housing

- Squatter Settlements

- Student Housing

- Vernacular Housing

- Zoning

- American Housing Survey

- Centrally Planned Housing Systems

- Colonias

- Global Strategy for Shelter

- Hedonic Pricing Model

- Hogan

- Household

- Housing Abroad: Africa

- Housing Abroad: Asia

- Housing Abroad: Canada

- Housing Abroad: Central and Eastern Europe

- Housing Abroad: Latin America

- Housing Abroad: Middle East

- Housing Abroad: Western and Northern Europe

- Housing Indicators

- Housing Markets

- Igloo

- Kibbutz

- Residential Satisfaction

- World Bank

- Exurbia

- Growth Machines

- Housing Bubble

- Housing Demand

- Housing Starts

- Housing Supply

- Infrastructure

- Levittowns

- McMansion

- Mixed-Use Development

- New Towns

- Open Space and Parks

- Real Estate Developers and Housing

- Smart Growth

- Space Standards

- Speculation

- Subdivision

- Subdivision Controls

- Suburbanization

- Blockbusting

- Discrimination

- Exclusionary Zoning

- Fair Housing Act

- Hispanic Americans

- Housing Courts

- Inclusionary Zoning

- Mount Laurel

- Predatory Lending

- Redlining

- Restrictive Covenants

- Right to Housing

- Segregation

- Eminent Domain

- Farmers Home Administration (Rural Housing Service)

- Federal Government

- Federal Housing Administration

- Government-Sponsored Enterprises

- HOPE VI

- Housing Act of 1949

- Housing Act of 1954

- Housing and Urban Development Act of 1968

- President's Committee on Urban Housing (Kaiser Commission)

- Real Estate Settlement Procedures Act of 1974

- Resolution Trust Corporation

- United States Census Bureau

- United States Department of Housing and Urban Development

- United States Department of Veterans Affairs

- Single-Parent Households

- Women as Housing Producers

- Women as Users of Housing

- Environment and Housing

- Environmental Contamination: Asbestos

- Environmental Contamination: Lead

- Environmental Contamination: Mold

- Environmental Contamination: Radon

- Environmental Contamination: Toxic Waste

- Environmental Hazards: Earthquakes

- Environmental Hazards: Flooding

- Environmental Hazards: Hurricanes

- Health Codes

- Indoor Air Quality

- Restoration of Damaged Housing

- Slums

- Homelessness

- Hoovervilles

- Single-Room Occupancy Housing

- Tent Cities

- Appraisal Industry

- First-Time Home Buyer

- Homeownership

- Liens

- Multiple Listing Service

- Property Rights

- Property Tax

- Refinancing

- Warranties

- Ancient Housing

- Automated Valuation Model

- Building Codes

- Computer-Aided Design

- Construction Technology

- Decision Models for Housing and Community Development

- Disaster-Resistant Housing

- Earth-Sheltered Housing

- Flexible Housing

- Housing Codes

- HUD Minimum Property Standards

- In Situ Construction

- Innovation in Housing

- Lean Construction

- Manufactured Housing

- Model Codes

- Modular Construction

- New Urbanism

- Operation Breakthrough

- Panic Room (Safe Room)

- Prefabrication

- Smart House and Automation Technologies

- Solar Housing

- Building Cycle

- Building Permit

- Consolidated Plans

- Home Improvement

- Housing Finance Agencies

- Landscape Architecture

- Maintenance

- Savings and Loan Industry

- Adjustable-Rate Mortgages

- Equity

- Mortgage Credit Certificates

- Mortgage Finance

- Mortgage Insurance

- Mortgage Revenue Bonds

- Mortgage-Backed Securities

- Negative Amortization

- Proposition 13

- Second Mortgage

- Subprime Mortgage Crisis

- Tax Expenditures

- Tax Incentives

- Accessory Dwelling Units

- Aging in Place

- Assisted Living

- Congregate Housing

- Continuing Care Retirement Communities

- Dementia

- Disabilities, Housing of Persons with

- Elderly

- Home Care

- Hospice Care

- Nursing Homes

- Retirement Communities

- Reverse-Equity Mortgage

- Second Homes

- Universal Design

- Depreciation of Property

- Lease

- Multifamily Housing

- Rent Control

- Rent Strikes

- Residential Hotels

- Residential Property Management

- Gautreaux Program

- Low-Income Housing Tax Credits

- Pruitt-Igoe

- Public Housing

- Public-Private Housing Partnership

- Demand-Side Subsidies

- Moving to Opportunity

- Supply-Side Subsidies

- Energy Conservation

- Green Building

- Housing Careers

- Shared-Equity Homeownership

- Tenure Sectors

- Adaptive Reuse

- Brownfields

- Community Reinvestment Act

- Gentrification

- High-Rise Housing

- Historic Preservation

- Homestead

- Incumbent Upgrading

- Infill Housing

- Mixed-Income Housing

- Model Cities Program

- Tax Increment Financing

- Urban Redevelopment

- Loading...

Get a 30 day FREE TRIAL

-

Watch videos from a variety of sources bringing classroom topics to life

Watch videos from a variety of sources bringing classroom topics to life -

Read modern, diverse business cases

-

Explore hundreds of books and reference titles

Read next

More like this

Sage Recommends

We found other relevant content for you on other Sage platforms.

Have you created a personal profile? Login or create a profile so that you can save clips, playlists and searches