Entry

Reader's guide

Entries A-Z

Subject index

Preferred Provider Organizations (PPOs)

A preferred provider organization (PPO) is a healthcare delivery system where providers contract with the PPO at various reimbursement levels in return for patient steerage into their practices and/or timely payment. PPOs differ from other healthcare delivery systems in the way they are financed as well as by providing more choice, benefit flexibility, and enrollee access to providers and medical services both in and out of network.

History

While PPOs have been in existence in some form or another for decades, the development of modern PPOs was the result of key legislative actions at the state and national level. In the 1970s and 1980s, many states passed enabling legislation to specifically allow for the development of PPOs. In 1974, the U.S. Congress enacted the Employee Retirement Income Security Act (ERISA). A very small portion of this law gave Taft-Harley Funds and other organizations the right to self-insure their healthcare benefits. Under the new law, organizations that self-insured would not be subject to various state coverage mandates or to state premium taxes; instead, they were now free to develop employee healthcare benefit programs. Recognizing the unique opportunity, third-party administrators began providing some or all of the services required by the self-insuring companies.

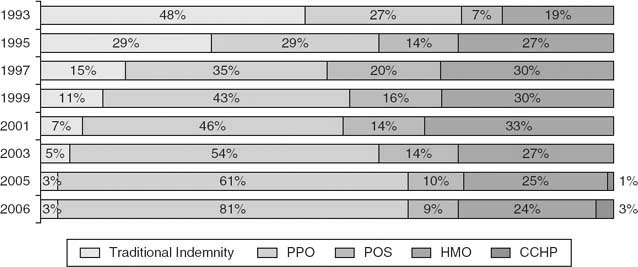

As a rule, however, these third-party administrators did not develop their own delivery networks and instead looked to another fledgling group of companies-preferred provider organizations-to credential and supply networks of physicians and healthcare institutions. Insured products grew and employers and other purchasers came to see PPOs as the middle ground between health maintenance organizations (HMOs) (traditionally lower cost but more restrictive) and indemnity insurance plans (permissive but more expensive). This fueled the development of local PPO organizations in the 1970s and 1980s and-beginning in the 1990s-encouraged the expansion of a limited number of national PPOs. The growth in PPO plan enrollment at the expense of traditional indemnity insurance and point of service plans is shown in Figure 1.

Today PPOs are tremendously popular. Over the past few years, there has been a consolidation of the PPOs marketplace resulting in fewer regional PPOs and larger national plans as regional plans merge or are bought by larger national plans.

In 2007, more than 158 million individuals were enrolled in a PPO program, which represents 64% of all Americans with healthcare coverage. One reason for this strong market share is that PPOs have delivered what the public has called for: choice, flexibility, and a balance between delivery of appropriate care and cost control.

Characteristics and Types of PPOs

There are two basic types of PPOs: a nonrisk PPO and a risk PPO. A nonrisk PPO's primary focus is to contract with providers in a geographical area to form an interconnected network of providers and services. The nonrisk PPO network leases and/or “rents” its network for a fee to insurance companies, self-insured employers, union trusts, third-party administrators, business coalitions, and associations. In contrast, a risk PPO assumes the financial risk for an enrollee's healthcare costs.

Figure 1 A Comparison of Medical Plan Enrollment, 1993 to 2006

...

- Access to Care

- Access to Healthcare

- Access, Models of

- Critical Access Hospitals (CAHs)

- Cultural Competency

- Direct-to-Consumer Advertising (DTCA)

- E-Health

- E-Prescribing

- Ethnic and Racial Barriers to Healthcare

- Geographic Barriers to Healthcare

- Health Communication

- Health Literacy

- Health Professional Shortage Areas (HPSAs)

- Healthcare Web Sites

- Hospital Closures

- Inner-City Healthcare

- Medical Travel

- National Health Service Corps (NHSC)

- Patient Dumping

- Patient Transfers

- Rural Health

- Safety Net

- Telemedicine

- Transportation

- Accreditation, Associations, Foundations, and Research Organizations

- Accreditation

- Associations

- AARP

- AcademyHealth

- America's Health Insurance Plans (AHIP)

- American Academy of Family Physicians (AAFP)

- American Academy of Pediatrics (AAP)

- American Association of Colleges of Nursing (AACN)

- American Association of Preferred Provider Organizations (AAPPO)

- American College of Healthcare Executives (ACHE)

- American Health Care Association (AHCA)

- American Health Planning Association (AHPA)

- American Hospital Association (AHA)

- American Medical Association (AMA)

- American Nurses Association (ANA)

- American Osteopathic Association (AOA)

- American Public Health Association (APHA)

- American Society of Health Economics (ASHE)

- Association of American Medical Colleges (AAMC)

- Association of University Programs in Health Administration (AUPHA)

- Healthcare Financial Management Association (HFMA)

- Institute for Healthcare Improvement (IHI)

- International Health Economics Association (IHEA)

- National Alliance for the Mentally Ill (NAMI)

- National Association of Health Data Organizations (NAHDO)

- National Association of State Medicaid Directors (NASMD)

- National Center for Assisted Living (NCAL)

- National Citizens' Coalition for Nursing Home Reform (NCCNHR)

- National Coalition on Health Care (NCHC)

- National Commission for Quality Long-Term Care (NCQLTC)

- National Health Policy Forum (NHPF)

- National Medical Association (NMA)

- National Quality Forum (NQF)

- University HealthSystem Consortium (UHC)

- Business Coalitions

- Foundations

- Research Organizations

- Biographies of Current and Past Leaders - Current Leaders

- Current Leaders

- Aday, Lu Ann

- Aiken, Linda H.

- Altman, Drew E.

- Andersen, Ronald M.

- Arrow, Kenneth J.

- Berwick, Donald M.

- Brook, Robert H.

- Chassin, Mark R.

- Clancy, Carolyn M.

- Culyer, Anthony J.

- Davis, Karen

- Drummond, Michael

- Ellwood, Paul M.

- Enthoven, Alain C.

- Evans, Robert G.

- Feder, Judith

- Fuchs, Victor R.

- Ginsburg, Paul B.

- Grossman, Michael

- Kane, Robert L.

- Katz, Sidney

- Lee, Philip R.

- Lomas, Jonathan

- Luft, Harold S.

- Marmor, Theodore R.

- Maynard, Alan

- Mechanic, David

- Naylor, C. David

- Newhouse, Joseph P.

- O'Leary, Dennis S.

- Pauly, Mark V.

- Reinhardt, Uwe E.

- Relman, Arnold S.

- Rice, Dorothy P.

- Roos, Leslie L.

- Roos, Noralou P.

- Rosenbaum, Sara

- Sackett, David L.

- Scott, W. Richard

- Shortell, Stephen M.

- Starfield, Barbara

- Starr, Paul

- Stevens, Rosemary A.

- Tarlov, Alvin R.

- Ware, John E.

- Wennberg, John E.

- White, Kerr L.

- Wilensky, Gail R.

- Past Leaders

- Anderson, Odin W.

- Cochrane, Archibald L.

- Codman, Ernest Amory

- Cohen, Wilbur J.

- Davis, Michael M.

- Donabedian, Avedis

- Eisenberg, John M.

- Farr, William

- Flexner, Abraham

- Ginzberg, Eli

- Kimball, Justin Ford

- McNerney, Walter J.

- Nightingale, Florence

- Roemer, Milton I.

- Rorem, C. Rufus

- Shapiro, Sam

- Sheps, Cecil G.

- Thompson, John Devereaux

- Williams, Alan H.

- Current Leaders

- Cost of Care, Economics, Finance, and Payment Mechanisms

- Administrative Costs

- Capitation

- Charity Care

- Committee on the Costs of Medical Care (CCMC)

- Compensation Differentials

- Cost Containment Strategies

- Cost of Healthcare

- Cost Shifting

- Cost-Benefit and Cost-Effectiveness Analyses

- Current Procedural Terminology (CPT)

- Diagnosis Related Groups (DRGs)

- Economic Barriers to Healthcare

- Economic Recessions

- Economic Spillover

- Economies of Scale

- Fee-for-Service

- Flat-of-the-Curve Medicine

- Health Economics

- Healthcare Financial Management

- Healthcare Markets

- Inflation in Healthcare

- Long-Term Care Costs in the United States

- Market Failure

- Pay-for-Performance

- Payment Mechanisms

- Pharmacoeconomics

- Prospective Payment

- Resource-Based Relative Value Scale (RBRVS)

- Supplier-Induced Demand

- U.S. National Health Expenditures

- Uncompensated Healthcare

- Disease, Disability, Health, and Health Behavior

- Activities of Daily Living (ADL)

- Acute and Chronic Diseases

- Adverse Drug Events

- Chronic-Care Model

- Diabetes

- Disability

- Disease

- Emerging Diseases

- Genetics

- Health

- Health Indicators, Leading

- Iatrogenic Disease

- Infectious Diseases

- International Classification of Diseases (ICD)

- Life Expectancy

- Medical Sociology

- Medicalization

- Mental Health

- Morbidity

- Mortality

- Mortality, Major Causes in the United States

- Obesity

- Pain

- Prescription and Generic Drug Use

- Tobacco Use

- Government and International Healthcare Organizations

- International Organizations

- Canadian Association for Health Services and Policy Research (CAHSPR)

- Canadian Health Services Research Foundation (CHSRF)

- Canadian Institute of Health Services and Policy Research (IHSPR)

- Pan American Health Organization (PAHO)

- United Kingdom's National Health Service (NHS)

- United Kingdom's National Institute for Health and Clinical Excellence (NICE)

- World Health Organization (WHO)

- U.S. Government Organizations

- Agency for Healthcare Research and Quality (AHRQ)

- Centers for Disease Control and Prevention (CDC)

- Centers for Medicare and Medicaid Services (CMS)

- Congressional Budget Office (CBO)

- Health Resources and Services Administration (HRSA)

- Indian Health Service (IHS)

- Medicare Payment Advisory Commission (MedPAC)

- National Center for Health Statistics (NCHS)

- National Guideline Clearinghouse (NGC)

- National Information Center on Health Services Research and Health Care Technology (NICHSR)

- National Institutes of Health (NIH)

- Substance Abuse and Mental Health Services Administration (SAMHSA)

- TRICARE, Military Health System

- U.S. Department of Veterans Affairs (VA)

- U.S. Food and Drug Administration (FDA)

- U.S. Government Accountability Office (GAO)

- International Organizations

- Health Insurance

- Adverse Selection

- Blue Cross and Blue Shield

- Carve-Outs

- Coinsurance, Copays, and Deductibles

- Consumer-Directed Health Plans (CDHPs)

- Crowd-Out

- Employee Health Benefits

- Flexible Spending Accounts (FSAs)

- Health Insurance

- Health Insurance Coverage

- Health Savings Accounts (HSAs)

- Medicaid

- Medicare

- Medicare Part D Prescription Drug Benefit

- Moral Hazard

- RAND Health Insurance Experiment

- Selective Contracting

- Single-Payer System

- State Children's Health Insurance Program (SCHIP)

- State-Based Health Insurance Initiatives

- Tax Subsidy of Employer-Sponsored Health Insurance

- Health Professionals and Healthcare Organizations

- Academic Medical Centers

- Allied Health Professionals

- Ambulatory Care

- Case Management

- Chiropractors

- Community Health Centers (CHCs)

- Community Mental Health Centers (CMHCs)

- Complementary and Alternative Medicine

- Dentists and Dental Care

- Disease Management

- Diversity in Healthcare Management

- Emergency Medical Services (EMS)

- Eye Care Services

- Federally Qualified Health Centers (FQHCs)

- Free Clinics

- General Practice

- Health Maintenance Organizations (HMOs)

- Health Systems Agencies (HSAs)

- Health Workforce

- Healthcare Organization Theory

- Home Health Care

- Hospice

- Hospital Emergency Departments

- Hospitalists

- Hospitals

- Intensive-Care Units

- Intermediate-Care Facilities (ICFs)

- Long-Term Care

- Managed Care

- Medical Group Practice

- Multihospital Healthcare Systems

- Nonprofit Healthcare Organizations

- Nurse Practitioners (NPs)

- Nurses

- Nursing Homes

- Pharmaceutical Industry

- Pharmacy

- Physician Assistants

- Physician Workforce Issues

- Physicians

- Physicians, Osteopathic

- Preferred Provider Organizations (PPOs)

- Primary Care

- Primary-Care Case Management (PCCM)

- Primary-Care Physicians

- Skilled-Nursing Facilities

- Health Services Research

- Data Sources in Conducting Health Services Research

- Health Services Research at the Veterans Health Administration (VHA)

- Health Services Research in Australia

- Health Services Research in Canada

- Health Services Research in Dentistry and Oral Health

- Health Services Research in Eastern Europe

- Health Services Research in Germany

- Health Services Research in Sub-Saharan Africa

- Health Services Research in the People's Republic of China

- Health Services Research in the United Kingdom

- Health Services Research Journals

- Health Services Research, Definition

- Health Services Research, Origins

- Laws, Regulations, and Ethics

- Measurement, Data Sources and Coding, and Research Methods

- Case-Mix Adjustment

- Causal Analysis

- Clinical Decision Support

- Cohort Studies

- Community-Based Participatory Research (CBPR)

- Computers

- Cross-Sectional Studies

- Data Privacy

- Data Security

- Diagnostic and Statistical Manual of Mental Disorders (DSM)

- Electronic Clinical Records

- Evidence-Based Medicine (EBM)

- General Health Questionnaire

- Geographic Information Systems (GIS)

- Health Informatics

- Health Surveys

- Healthcare Cost and Utilization Project (HCUP)

- Healthcare Effectiveness Data and Information Set (HEDIS)

- Healthcare Informatics Research

- Measurement in Health Services Research

- Meta-Analysis

- Minimum Data Set (MDS) for Nursing Home Resident Assessment

- National Practitioner Data Bank (NPDB)

- ORYX Performance Measurement System

- Provider-Based Research Networks (PBRNs)

- Quality of Well-Being Scale (QWB)

- Randomized Controlled Trials (RCTs)

- Satisfaction Surveys

- Severity Adjustment

- Short-Form Health Surveys (SF-36, -12, -8)

- Outcomes of Care

- Policy Issues, Healthcare Reform, and International Comparisons

- Comparing Health Systems

- Competition in Healthcare

- Equity, Efficiency, and Effectiveness in Healthcare

- Focused Factories

- For-Profit Versus Not-for-Profit Healthcare

- Forces Changing Healthcare

- Health Disparities

- Healthcare Reform

- International Health Systems

- National Health Insurance

- National Healthcare Disparities Report (NHDR)

- Public Policy

- Rationing Healthcare

- Technology Assessment

- Public Health

- Quality and Safety of Care

- Accreditation

- Benchmarking

- Clinical Practice Guidelines

- Continuum of Care

- Credentialing

- Geographic Variations in Healthcare

- International Classification for Patient Safety (ICPS)

- Malpractice

- Medical Errors

- National Healthcare Quality Report (NHQR)

- National Patient Safety Goals (NPSG)

- Nursing Home Quality

- Patient Safety

- Patient-Centered Care

- Quality Enhancement Research Initiative (QUERI) of the Veterans Health Administration (VHA)

- Quality Improvement Organizations (QIOs)

- Quality Indicators

- Quality Management

- Quality of Healthcare

- Quality of Life, Health-Related (HRQOL)

- Quality-Adjusted Life Years (QALYs)

- Structure-Process-Outcome Quality Measures

- Timeliness of Healthcare

- Special and Vulnerable Groups

- Loading...

Get a 30 day FREE TRIAL

-

Watch videos from a variety of sources bringing classroom topics to life

Watch videos from a variety of sources bringing classroom topics to life -

Read modern, diverse business cases

-

Explore hundreds of books and reference titles

Read next

More like this

Sage Recommends

We found other relevant content for you on other Sage platforms.

Have you created a personal profile? Login or create a profile so that you can save clips, playlists and searches