Entry

Reader's guide

Entries A-Z

Subject index

Microlending Programs

Microlending programs are one form of microfinance that includes savings, insurance, and other financial services for people considered too enmeshed in poverty to be served by traditional banking systems. Most microlending programs began as nongovernmental organizations in developing nations that relied on government grants and charitable support to sustain operations, and accordingly, the goals of microlending programs go beyond the financial. Advocates of these programs consider microlending to be a new way of looking at poverty alleviation and social change. by providing access to small loans at modest interest rates, microlending programs intend to unlock the entrepreneurial energies of the poor to increase human capital among the poor and improve civic engagement by the poor.

The contemporary form of microlending is attributed to the pioneering efforts of the 2006 Nobel Prize-winning Muhammad Yunus and the institution he founded in Bangladesh, Grameen Bank. Microlending programs have grown exponentially since the first personal loans Yunus offered to local villagers in the 1970s. The Microfinance Information Exchange, Inc. (MIX), a U.S. nonprofit organization that collects and analyzes global microfinance data, claims to collect data from 80 percent of microfinance institutions in the world. In 2011, MIX reported 95.1 million borrowers at 1,365 microfinance institutions. The outstanding loans totaled $87 billion with significant regional variation from a low average of $153 per borrower in south Asia to a high average of $1,862 per borrower in eastern Europe and central Asia.

Group Lending

Conventional bank lending to low income individuals without stable incomes or assets to use for collateral are rarely available to the clientele who are the focus of microlending programs. The classical method of overcoming individual credit risk deficiencies in microlending is group lending. In the Grameen Bank approach, five individuals self-organize into a group in which individual loans are staged over time. Repayments are scheduled at frequent intervals and processed in public meetings. Using this methodology has been highly effective, with more than 98 percent of loans being repaid in a timely manner in many countries. Economists note that self-organizing into groups makes use of local knowledge about borrower intent to repay; that modest degrees of joint liability among group members promote peer monitoring that helps prevent default; and that public repayment enhances social cohesion and can lead to effective social sanctions that promote repayment.

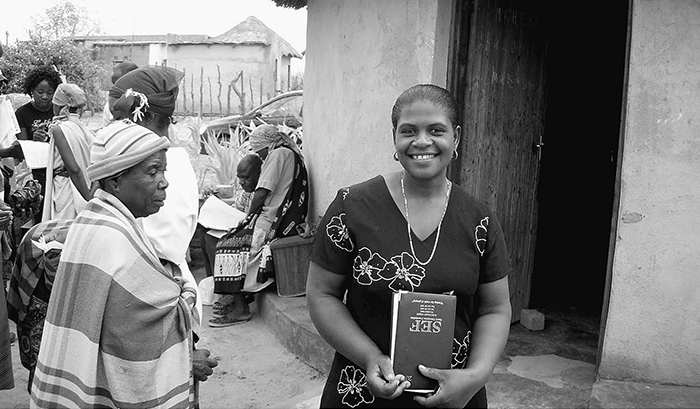

A loan officer from the GiveWell visits the nongovernmental organization the Small Enterprise Foundation in Tzaneen, South Africa, in 2010. The financial empowerment of women in poverty is perceived by many microlenders as the best means of achieving the social objectives associated with microfinance.

Gender Diversity

Women are overrepresented among the poorest of the poor in almost every nation, are frequently more focused on within-household financial needs than their male counterparts, and are generally considered to be exceptionally committed to the health and education of their children. The financial empowerment of women in poverty is perceived by many microlenders as the best means of achieving the social objectives associated with microfinance. No organization more strongly demonstrates the focus on gender diversity than the Microcredit Summit Campaign, with the goal of extending credit to 175 million of the world's poorest households by 2015. More than 78 percent of the loans reported through 2011 by the 720 cooperating microfinance institutions were made to women borrowers.

...

- Children and Youth Services

- Abandonment

- Abduction

- Abuse and Neglect

- Adolescent/Youth Services: Overview

- Adoption Agencies and Services

- Adoption, Special Needs

- Adoption: Infants, International, and Older/Special Needs Children

- Aftercare Services for Children Aging Out of Foster Care

- Aggression Replacement Training

- AMBER Alert

- Ansell-Casey Life-Skills Assessment

- At-Risk Youth Services

- Behavior Modification and Residential Treatment Facilities Behavior Support and Management Biracial Children

- Boarder Babies

- Boot Camps

- Bullying

- Child Abuse/Neglect, Victims of

- Child and Adolescent Needs and Strengths

- Child Protective Services

- Child Support Agencies and Services

- Child Welfare Services

- Children in Foster Care

- Children in Special Living Arrangements

- Children of Incarcerated Parents

- Children of Substance Abusers

- Children of Undocumented Aliens

- Children, Youth and Human Trafficking

- ChildStats

- Continuum of Care

- Daniel Memorial Institute System Independent Living Skills

- Day Care for Children

- Disposition of Juvenile Records

- Early Childhood Development

- Early Childhood Literacy

- Education and Training Vouchers

- Educational Support Services

- Families, Nontraditional

- Family Crisis Intervention Planning

- Family Permanency Planning

- Fetal Alcohol Syndrome and Drug-Exposed Infants

- Foster Care Agencies

- Gangs in Schools

- Genogram

- Group Homes for Children

- Head Start and Prekindergarten Programs

- Immunization Campaigns

- Infant Mortality/Sudden Infant Death Syndrome

- Infant/Toddler Development

- Intelligence Testing

- Interethnic Adoption Provision

- Jail Diversion Programs for Children and Adolescents

- Juvenile Justice System

- KIDS COUNT

- Kinship Care

- Life Book

- Life Skills Training

- Maternity Homes

- Monitoring the Future

- Multicultural Education Journals

- Multiracial Children

- Multisystemic Therapy

- National Center for Children in Poverty

- National Child Abuse and Neglect Data System

- National Survey of Family Growth

- National Youth in Transition Database

- Parenting Skills Training

- Parenting Styles, Cultural Differences in

- Paternity, Establishing

- Peer Pressure

- Profile of Parenting Study

- Protective Services for Children

- Runaway Youth

- School Counselors

- School Mental Health Project

- School Psychologists

- School Social Workers, Racial and Ethnic Issues for

- Special Education

- State Children's Health Insurance Program Status Offense

- Substance Abuse Treatment for Children and Adolescents Targeted Case Management Truancy

- Youth Risk Behavior Surveillance System

- Zero Tolerance Approach in Schools

- Community Development

- Administration for Community Living

- After-School Services

- Business Incubator

- Community Action Agencies

- Community Corrections

- Community Development Block Grants

- Community Development Corporations

- Community Health Centers

- Community Organizing

- Community-Based Services

- Cultural Services

- Educational Services

- Eminent Domain

- Enterprise Zone

- Fair Lending Practices

- Gentrification

- Grassroots Leadership

- Habitat for Humanity

- Health Promotion Services

- Housing Services

- Microlending Programs

- Neighborhood Watch Programs

- NeighborWorks America

- Policing and Safety

- Primacy of Place

- Prisoner Reentry Programs

- Recreation Services

- Redlining

- Section 8

- Senior Services

- Transportation Services

- Volunteer Services

- Cultural Competence in Human Services

- Code of Ethics of the National Association of Social Workers

- Diversities

- Diversity and Equality in Health Care

- Journal Ethnic and Cultural Diversity in Social Work

- Journal of Human Services

- Journal of Immigrant and Minority Health

- American Academy of Social Work and Social Welfare

- Changing the Client Versus Changing the Environment

- Childhood Trauma

- Colonialism, Lingering Effects of

- Communication Styles, Ethnic and Cultural Differences in

- Community-Based Participatory Research

- Critical Race Theory

- Cross-Cultural Knowledge

- Cross-Cultural Service Models

- Cross-Cultural Skills

- Cultural Competence, Human Service Providers and

- Cultural Competence, Measuring and Assessing

- Cultural Competence, Model of

- Cultural Competence, Professional Standards of

- Cultural Competence, Training in

- Cultural Humility, Model of

- Cultural Paradigms

- Culturally Diverse Practice, Definitions of

- Culturally Diverse Practice, Theories of

- Culturally Specific Services

- Death and Dying, Cultural Attitudes Toward

- Diversity in the Workplace

- Education for Diversity in Human Services

- Emic and Etic

- Empowerment Research

- Ethnocentrism and Ethnorelativism

- Executive Orders

- Factline: Tracking Health in Underserved Communities

- Implicit Bias

- Institute for Women's Policy Research

- Institutional Oppression

- Intangible Cultural Heritage

- Interprofessional and Interdisciplinary Practice

- Levels of Intervention

- Life Course Approach

- Locus of Control, Cultural Differences in

- Marriage and Family Therapists

- Medicine, Workforce Diversity in

- Multicultural Education

- Personal Practice, Model of

- Power, Race/Ethnicity and

- Prejudice, Theories of

- Providers, Institutional Racism and

- Racial Microaggression

- Racism, Long-Term Effects of

- Racism, Self-Assessment of

- Service Providers and Diversity

- Social Determinants of Health

- Social Epidemiology

- Social Innovation

- Social Work Practice and People of Color

- Social Work, Diversity Practice in

- Social Workers

- Sociology of Disability

- Spirituality/Religion and Diversity

- Culture-Specific Services

- Ableism

- ADHD, Services for Individuals With

- Age and Clients

- Aging and Adult Services

- Assistive Technology

- Autism and Asperger's Syndrome, Services for

- Blindness and Low Vision

- Children With Special Needs

- Children, Youth, and Human Trafficking

- Cisgender

- Cultural Broker

- Deaf/Hard of Hearing

- Developmental Disabled Individuals

- Disability Services

- Disability Studies

- Disabled Clients

- Elder Care/Geriatric Services

- Families of Prisoners and Ex-Prisoners

- Fundamentalist Christian Americans

- Gangs, Social Issues of and Intervention

- Gender and Clients

- Heterosexual Privilege

- Immigrant Populations, Human Service Needs of

- Immigration: Human Service Issues

- Interfaith Couples

- Juvenile Delinquents

- Juvenile Detention Centers

- Learning Disabilities, Services for Individuals With

- LGBTQ Clients

- Longitudinal Studies of Aging

- Marriage and Family Therapy

- Meaningful Access

- Mobility-Impaired Individuals

- Mormons

- National Institute on Aging

- Neurodiversity

- Prisoners and Ex-Prisoners

- Probation and Parole Officers

- Protective Services for Adults

- Reasonable Accommodations

- Religion and Clients

- Same-Sex Marriage/Couples

- Sexual Abuse Survivors

- Sexual Reassignment Surgery

- Size Discrimination

- Social Services, Disabled Children and

- Student Visas

- Subcultures

- Torture, Survivors of

- Transgender Individuals

- Two-Spirits

- Universal Access/Universal Design

- Victim Services

- War and Terrorism, Survivors of

- Women, Battered

- Family Services

- Alloparenting, Cultural Aspects of

- Co-Parenting, Cultural Aspects of

- Counseling and Psychotherapy Services

- Divorce

- Domestic Violence, Victims of

- Economic Support and Services

- Emergency Fuel Services

- Employment/Career Assistance Services

- Family Planning Services

- Family Preservation Services

- Family Services

- Family Violence Prevention and Services

- Food Support

- Housing Support and Homeless Services

- Kinship Care, Cultural Aspects of

- Legal Services

- Respite Services

- Wraparound Services/Systems of Care

- Hospitals, Health Care, and Cultural Competence

- Adult Day Care

- AIDS/HIV Programs

- Case Management Services

- College and University Health Services

- Communication Disorders, Services for

- Community Health, Racial and Ethnic Approaches to

- Dental Services

- Directly Observed Therapy

- Do Not Resuscitate Order

- Emergency Medical Care

- Harm Reduction Programs

- Health as a Human Right

- Health Care Delivery, Models of

- Health Care, Disparities in

- Health Insurance

- Home and Community Services

- Home Care Services

- Hospice Services

- Hospitals

- Immunization

- Maternal/Infant Health Services

- Medicaid

- Medical Necessity

- Medical Social Workers, Racial and Ethnic Issues for

- Medical Supplies, Access to

- Medical Transportation

- Medicare

- Meditation/Yoga

- Midwifery

- National Health and Nutrition Examination Survey

- National Healthcare Disparities Reports

- Neonatal Care

- Nursing Home Care

- Nursing, Public Health

- Nutritional Services and Assessment

- Occupational Therapy

- Outpatient Medical Care

- Overweight and Obese Adults and Children

- Pain Management

- Palliative Care

- Partner Notification Programs in HIV/AIDS

- Pharmaceuticals, Access to

- Pregnancy and Parenting Services

- Prenatal Care

- Public Health

- Quality of Life, Measuring of

- Racial and Ethnic Approaches to Community Health

- Rehabilitative Services

- Respite Care

- School Health Services

- Telecommunications Devices for the Deaf

- Workplace Health Services

- International Cultural Competence

- Alcohol Consumption, International Variations in Attitudes Toward

- Alternative Medical Systems

- Child Labor, International Variations in Attitudes Toward

- Children and War

- Children, International Variations in Attitudes Toward

- Chronic Diseases Common in Developing Countries

- Coca-Colonization

- Communicable Diseases Common in Developing Countries

- Cultural Appropriation

- Diaspora

- Disabilities, International Variations in Attitudes Toward

- Domestic Violence, International Variations in Attitudes Toward

- Family Reunification

- Family, International Variations in Definitions of

- Female Genital Mutilation

- Gender Issues and Roles in Developing Countries

- Gender Issues and Roles in Non-Western Countries

- Global Burden of Disease

- Health and Sickness, Differing Attitudes Toward

- Help-Seeking Behavior, Cultural Differences in

- Honor Killings

- Human Trafficking

- ICE Detention Centers, Services in

- Infanticide, International Variations in Attitudes Toward

- International Adoptions and Families

- International Federation of Social Workers

- Mental Health, International Variations in Attitudes Toward

- Missionary Work and Workers

- Natural Disasters, Service for

- Naturalized Citizens

- Pandemics

- Poverty

- Rape as an Instrument of War

- Refugee Assistance

- Reparations

- Rites of Passage

- Role Flexibility, International Differences in

- Sweatshop Laborers

- Tobacco Use, International Variations in Attitudes Toward

- Traditional Medicine

- Legislation and Regulations

- Adoption and Foster Care Analysis and Reporting System

- Adoption and Safe Families Act

- Americans with Disabilities Act

- Americans with Disabilities Act of 1990

- Child Abuse Prevention and Treatment Act

- Community Reinvestment Act (1977)

- Convention on the Rights of Persons with Disabilities, United Nations

- Cultural and Linguistically Appropriate Services Standards

- DREAM Act, The

- Equal Pay Act of 1963

- Fair Labor Standards Act

- Family Violence Prevention and Services Act

- Fostering Connections to Success and Increasing Adoptions Act of 2008

- Health Insurance Portability and Accountability Act of 1966

- Indian Child Welfare Act

- Indian Civil Rights Act of 1968

- Individuals with Disabilities Education Act

- Interstate Compact for Juveniles

- Interstate Compact on the Placement of Children

- McKinney-Vento Homeless Education Assistance Improvements Act of 2001

- Multiethnic Placement Act of 1994

- No Child Left Behind Act

- TRIO Programs

- United Nations Convention on the Prevention and Punishment of the Crime of Genocide

- United Nations Convention on the Rights of the Child

- United Nations Declaration on the Rights of Indigenous Peoples

- Universal Declaration of Human Rights

- Voting Rights Act of 1965

- Mental and Behavioral Health Services

- Diagnostic and Statistical Manual of Mental Disorders, Cultural Responsiveness of

- Alcohol and Substance Abuse Services

- Autism Diagnostic Observation Schedule

- Behavioral Health Disparities for Racial and Ethnic Minority Populations

- Case Management

- Chemical Restraints

- Conflict Resolution and Diversity

- Crisis Services

- Day Treatment Centers

- Deinstitutionalization

- Developmental Disabilities, Attitudes and Myths in Services for

- Drug and Alcohol Screening

- Eating Disorders, Cultural Aspects of

- Employee Assistance Programs

- Ethnic Groups and Drug and Alcohol Use

- Face-Blindness (Prosopagnosia)

- Family Therapy

- Gambling Addictions

- Genetic Counseling, Cultural Aspects of

- Group Homes for Adults

- Group Therapy

- Information and Referral

- Interpersonal Violence

- Long-Term Residential Care

- Marriage Counseling

- Mental Health Service Delivery, Cultural Characteristics

- Mental Health Services, Adult

- Mental Health Services, Child

- Mental Health Services, Ethnic Models and Multicultural

- Military Families

- Military Personnel

- Military Veterans

- National Database for Autism Research

- National Institute of Mental Health

- Native Americans, Suicide Among

- Partial Care Services for Adults, Mental Health

- Partial Care Services for Children, Mental Health

- Peer Support and Counseling Services

- Postpartum Depression

- Psychiatric/Psychological Assessment

- Rehabilitation Centers

- Restorative Justice

- Self-Harm, Cultural Aspects of

- Smoking and Smoking Cessation, Cultural Aspects of

- Substance Abuse and Mental Health Services Association

- Suicide Prevention Services

- Suicide, Cultural Aspects of

- Supported Housing

- Trauma-Focused Services

- Twelve-Step Programs

- Veterans Services

- Organizations, Programs, Government Agencies, and Departments

- Administration for Native Americans

- Administration on Children, Youth and Families

- Administration on Intellectual and Developmental Disabilities

- Agency for Healthcare Research and Quality

- American Correctional Association

- Asian and Pacific Islander American Health Forum

- Association for Multicultural Counseling and Development

- Association of Administrators of the Interstate Compact on the Placement of Children

- Association of Juvenile Compact Administrators

- Child Welfare League of America

- Children's Defense Fund

- Court-Appointed Special Advocate, National Association

- Department of Education, U.S.

- Department of Health and Human Services, U.S.

- DiversityRx

- Enterprise Community Partners

- Human Capital Development Initiative

- Institute of Education Sciences

- International Mental Health Research Organization

- John H. Chafee Foster Care Independence Program

- Joint Commission, The

- Low-Income Housing Tax Credits

- Mental Health Gap Action Program

- National Alliance for Hispanic Health

- National Assessment Governing Board

- National Center for Cultural Competence

- National Center for Hate Crime Prevention

- National Center for Missing and Exploited Children

- National Center on Minority Health and Health Disparities

- National Congress of American Indians

- National Mental Health Association

- National Minority AIDS Council

- National Organization for Human Services

- Neighborhood Reinvestment Corporation

- Office for Civil Rights

- Office for Faith-Based and Neighborhood Partnerships, White House

- Office of Juvenile Justice and Delinquency Prevention

- Office of Safe and Drug-Free Schools

- Office of Special Education and Rehabilitative Services

- Social Security Administration

- TuDiabetes

- U.S. Citizenship and Immigration Services

- U.S. Immigration and Customs Enforcement

- United Nations High Commissioner for Refugees

- Yale Center for Dyslexia and Creativity

- Race and Ethnicity

- Regional Cultural Competence

- Accommodation

- Acculturation

- African Americans

- African Immigrants

- Alaskan Natives

- American Indian Movement

- Anti-Semitism

- Antilocution

- Appalachia and Human Services

- Arab Americans

- Asian Americans

- Asian Immigrants

- Asian Indian Immigrants

- Assimilation

- Bias in Service Delivery

- Biculturalism

- Biracial Couples

- Blue Vein Society/Paper Bag Test

- Border Communities

- Caribbean Immigrants

- Center for Native American Youth

- Central American Immigrants

- Chinese Americans

- Conflict Resolution and Diversity

- Cuban Americans

- Cultural Determinism

- Cultural Literacy

- Discrimination and Institutional Racism

- Displaced Persons

- Dominican Americans

- Environmental Racism

- Equal Opportunity and Civil Rights

- Ethnic Diversity and Values

- Ethnicity and Clients

- Ethnicity, Definitions of

- Ethnocentrism

- European Americans

- Filipino Americans

- Global South/Global North

- Haitian Americans

- Hate Groups

- Hawai'ian Native Americans

- Hispanic Americans

- Hispanic Health and Nutrition Examination Survey

- Hispanic Immigrants

- Hmong Immigrants

- Holocaust Survivors

- Immigration Law: History of U.S.

- Incarceration and Sentencing, Racial Disparities in

- Indian Boarding Schools

- Indian Health Service

- Internal Revenue Service's Migration Data Files

- Isolated Communities and Cultural Competence

- Jewish Americans

- Language Assistance

- Literacy Testing

- Melting Pot Theory

- Mexican Americans

- Migrant Workers

- Model Minority Stereotype

- Monoculturalism

- Multiculturalism

- Multiracial Individuals and Families

- Muslim Americans

- Native Americans

- Office of Refugee Resettlement

- Pacific Islander Immigrants

- Pacific Islanders

- People of Color: Service Delivery, Psychological Assessment, Cultural Issues

- Pluralism

- Puerto Ricans

- Race and Clients

- Race, Social Definitions of

- Racial and Ethnic Categories, U.S. Census

- Racial Identity Development, Models of

- Regional Cultural Competence

- Reverse Discrimination

- Rural Communities

- Self-Determination and Educational Assistance Act

- Sikhism

- Slavery and Lasting Cultural Effects of Social Biology/Biological Determinism

- Social Darwinism

- South American Immigrants

- Southern Communities and Cultural Competence

- Stolen Generation

- Tribal Social Services

- Tribal Sovereignty

- U.S. Cultural Regions

- Undocumented Immigrants

- United Farm Workers of America

- United States, Demographics of

- Urban Communities and Human Services

- Values, Ethics, Ethnic Diversity and

- Vietnamese Americans

- Western Communities and Cultural Competence

- White Privilege

- Women Minorities

- Socioeconomic Status and Cultural Competence

- Adult Education Programs and Services

- Adult Literacy Programs

- Aid to Families with Dependent Children, Historical Role of

- Blue Collar/Pink Collar/White Collar

- Cultural Capital, Role of

- Dual Income, No Kids

- Educational Status and Service Delivery

- Environmental Justice

- Family Structure, Diversity of

- Financial Literacy Programs

- Food Desert

- Food Insecurity

- Health Disparities, Role of

- Homelessness

- Linguicism

- National Urban League

- Personal Responsibility and Work Opportunity Reconciliation Act

- Single Parents

- Social and Economic Justice

- Social Capital, Role of

- Social Security, Services Funded by

- Social Welfare Policy, Cultural Competence in

- Social Welfare Programs, Cultural Competence in

- Socioeconomic Status

- Supplemental Security Income, Services Funded by

- Temporary Aid to Needy Families

- Uninsured Clients

- War on Poverty Programs

- Welfare Reform, Role of

- Yuppies and Buppies

- Loading...

Get a 30 day FREE TRIAL

-

Watch videos from a variety of sources bringing classroom topics to life

Watch videos from a variety of sources bringing classroom topics to life -

Read modern, diverse business cases

-

Explore hundreds of books and reference titles

Read next

More like this

Sage Recommends

We found other relevant content for you on other Sage platforms.

Have you created a personal profile? Login or create a profile so that you can save clips, playlists and searches