Entry

Entries A-Z

Supply-Side Policies

A theory of economic stabilization that maintains that changes in aggregate supply rather than in aggregate demand are the major determinants of inflation, unemployment, and economic growth. Therefore, supply-siders argue that government policies that are intended to achieve stable prices and increased output must be targeted toward economic variables that can increase output and employment, such as the expansionary fiscal policy of tax reduction.

Supply-side economics presents tax reduction as an incentive to improve the work ethic and encourage saving and investment. The basic point of reference for tax evaluation is the marginal tax rate (the rate that is paid on the last unit of taxable income). Since the incentive to work, according to supply-siders, is highly contingent on disposable income (income after taxes), high marginal tax rates discourage worker productivity and put a tremendous burden on employers to invest, innovate, or employ more workers. Additionally, higher marginal tax rates are generally perceived by this school of thought to lead to tax avoidance and evasion—the obvious implication being a reduction in the tax revenue base as marginal tax rates reach prohibitive levels.

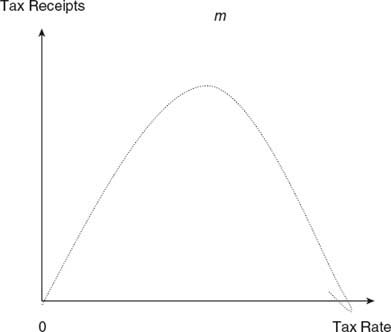

The tax Laffer curve (after the work of Arthur Laffer, but the concept antedates him by centuries; see Figure 1) is one of the widely used illustrations of the arguments of supply-siders, although there are substantial reservations about its accuracy.

Figure 1Laffer Curve

According to the Laffer parabola, tax receipts increase with the tax rate up to a certain critical point (m), after which there is an inverse relationship between tax rates and tax receipts. Beyond point m, as tax rate increases, tax receipts fall. The Laffer proposition, which was developed in the 1980s, seemed to explain economic performance reasonably well during the Kennedy and Reagan tax cuts of the 1960s and 1980s, but critics of the Laffer curve are apprehensive about the sensitivity of incentives to changes in the tax rate, particularly if tax incentives are poorly targeted.

Inasmuch as tax cuts can be beneficial to economic performance, Keynesians recommend tax cuts that will stimulate aggregate demand rather than aggregate supply, but the effects of tax cuts may well be indistinguishable if and when they are beneficial to both aggregate demand and supply—increasing workers' incentive to be productive on the one hand and increasing household disposable income on the other.

However, the empirical evidence of the Laffer argument is ambivalent. Workers tend to react to tax incentives differently—some preferring to work harder, while others increase their leisure time. Other concerns about the accuracy of the Laffer argument involve the appropriate timing of tax reductions (since policies might be susceptible to time lags, which can neutralize the intended outcomes of policy decisions) and the local maximum or optimum of tax receipts on the Laffer curve. For more information, see Mankiw (2006) and McConnell and Brue (2008).

Get a 30 day FREE TRIAL

-

Watch videos from a variety of sources bringing classroom topics to life

Watch videos from a variety of sources bringing classroom topics to life -

Read modern, diverse business cases

-

Explore hundreds of books and reference titles

Read next

More like this

Sage Recommends

We found other relevant content for you on other Sage platforms.

Have you created a personal profile? Login or create a profile so that you can save clips, playlists and searches