Entry

Entries A-Z

Equilibrium

A state of equality or balance in which economic variables and/or constants are equal or reflective of market expectations. The concept of equilibrium is central to economic analysis on three levels—individual decision making, market performance, and the macroeconomy (national economy). Individuals make decisions about how to spend limited income to balance the consumption of desired goods in order to maximize utility. Consumers are in equilibrium when the marginal utility of the last unit of money spent on one good is the same for all goods consumed.

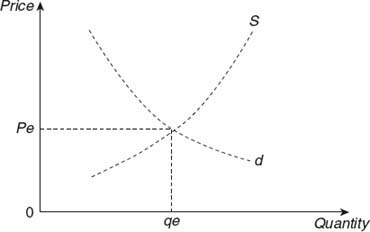

Markets are in equilibrium when the expected quantity of goods, services, assets, and inputs demanded (d) is equal to the expected supply (s). The estimated price and quantity at which supply is equal to demand are known as the equilibrium price (pe) and quantity (qe), respectively (see below).

Consumers and private investors demand finished products and assets, while businesses demand both inputs and assets in the factor (input) and financial markets. Private and institutional investors can also sell assets in financial markets at mutually agreeable (equilibrium or market) prices.

Equilibrium

The macroeconomy is in equilibrium when aggregate demand is equal to aggregate supply. Although equilibrium suggests a balance, not all equilibrium is desirable or stable. For example, a national economy might attain equilibrium, a point at which policy implementation can lead to an improved outcome of increased output and lower prices. It is also possible that shocks can destabilize a prevailing equilibrium. For more information, see McConnell and Brue (2008) and Schiller (2006).

Get a 30 day FREE TRIAL

-

Watch videos from a variety of sources bringing classroom topics to life

Watch videos from a variety of sources bringing classroom topics to life -

Read modern, diverse business cases

-

Explore hundreds of books and reference titles

Read next

More like this

Sage Recommends

We found other relevant content for you on other Sage platforms.

Have you created a personal profile? Login or create a profile so that you can save clips, playlists and searches