Whrrl: Facilitating Agricultural Finance through Block-Chain Technology

Case

Teaching Notes

Supplementary Resources

Abstract

The Indian agricultural financial market is currently underdeveloped due to the perceived high risk associated with rural and agricultural sectors by the formal financial sector. Warehouse receipt financing (WHR financing) offers access to working capital by allowing loans against deposited goods, but it faces security and efficiency issues, including fraudulent activities. These issues have concerned banks and other stakeholders. The transaction processes are manual, time-consuming, and lack transparency. In this context, technological innovations have the potential to transform financial markets, reducing risks and transaction costs. Whrrl, a blockchain-based platform, aimed to address security and inefficiency issues in asset-backed lending, specifically in Warehouse Receipt Financing. It consists of a blockchain platform connecting warehouses and banks at the backend and a mobile app for farmers and traders to interact with warehouses and banks. The Indian government introduced regulatory changes in June 2020 to support farmers. This prompted Ashish Anand and his team at Whrrl to consider their future steps. Whrrl aspired to expand beyond geographical and sector-based boundaries and become a global solution for asset-backed lending, particularly in South East Asia for commodities like agricultural cash crops, metals, crude oil, and Africa for agricultural products. However, challenges included slower market development in India and lower margins in Indian agricultural warehouse financing compared to other types of financing. The policy changes in the agricultural market presented new opportunities for Whrrl to become a significant player in agricultural trading as a trading platform for agricultural produce. This shift would require resources and a shift in expertise from technology solutions for asset-backed lending to the operations of agricultural trading.

This case study is provided in this Sage Business collection primarily as a basis for classroom discussion or self-study and is not meant to illustrate either effective or ineffective management styles. Nothing herein shall be deemed to be an endorsement of any kind. This case study is for scholarly, educational, or personal use only within your university, and cannot be forwarded outside the university or used for other commercial purposes.

© 2026 Sage Publications, Inc. All Rights Reserved.

Resources

| Exhibit 1 WHRLL’s Value Proposition | ||||

|---|---|---|---|---|

S. No. | Features | Beneficiary | Value proposition | Advantages over traditional process |

1 | Immutability | Lenders | Security: Records were reserved and could not be changed unless change was initiated by the controlling authority. | Traditional processes, involving multiple parties and platform, were prone to manual error as well as fraud. |

2 | Propagation Layer | Multi Stakeholders (Farmers, Banks, Warehouses) | Efficiency & simplification: All applications and transactions on farmer’s app (off-blockchain) and on block chain automatically communicated with each other. | Traditional processes were manual therefore took more time and effort. |

3 | Modular API Infrastructure | Warehouses & Banks | Decentralization & transparency: Data does not have to rely on centralized node, gets recorded, stored and updated through blockchain’s distributed ledger technology (DLT) | Traditional processes passed through centralized NERL |

4 | Smart contract | Warehouses & Banks | Efficiency & trust: Auto-executing commands that removed the need for human interference. Every action on WHR updated the smart contract to reflect the latest changes, visible via the Explorer at all times. Going forward, the smart contracts would take live commodity prices from the price oracle to initiate certain intended actions - all with the trust of a decentralized system. The behaviour mimicked that of legal contracts, and formulated a participant’s right and obligation on their digital assets. | |

5 | Digital farmers’ application | Farmers | Access & convenience: In-house discovery platform for detecting warehouse location and storage availability. This was available to farmers on their mobile phone. | Traditional processes were manual therefore took more time and effort and involved the depositor physically making rounds of the warehouses. |

6 | Digital loan application | Access, efficiency & simplification: Farmers could file for loan application online. | Traditional processes were manual therefore took more time and effort and involved the borrower physically visiting the banks. | |

7 | 100% electronic | Efficiency: Connected warehouses, banks and depositors. | Traditional processes were manual or email driven therefore took more time and effort. | |

8 | Digital KYC | Efficiency: Connected banks and customers electronically. | Traditional processes were manual or email driven therefore took more time and effort. | |

9 | Zero knowledge proof (Not built) | Anonymity: Recorded bank transactions to prove its existence without revealing its details/features to others. | ||

10 | Trading platform through tradable tokens | Tradability: Tradable tokens were generated for each deposit. Traders could get aggregated information about different warehouses. Banks could sell the depositors produce in case of default. | Traditional processes did not involve any such tokens to facilitate trade or recovery in case of default. | |

11 | IoT devices | Traceability & security: The blockchain reliably stored the communication of smart (hardware) devices as part of collateral management within the internet of things. | Absence of these devices resulted in frauds. | |

| Exhibit 2 Whrrl’s Transactions Before the Pandemic | |||

|---|---|---|---|

Metrics | 2020 | ||

Jan | Feb | Mar | |

States | 1 | 1 | 1 |

No. of Locations | 5 | 5 | 5 |

No. of Warehouses | 16 | 16 | 16 |

No. of Banks | 2 | 2 | 2 |

eWHR Generated (Rs. Cr.) | 1 | 7 | 16 |

Govt | - | 5 | 13 |

Farmers | 0 | 1 | 1 |

Agri Traders | 1 | 2 | 2 |

Co-operative Societies | - | - | - |

Other Entities | - | 0 | 0 |

Quantity (MT) | 249 | 1092 | 2751 |

Govt. | - | 564 | 1806 |

Farmers | 55 | 202 | 291 |

Agri Traders | 194 | 318 | 643 |

Co-operative Societies | - | - | - |

Other Entities | - | 9 | 11 |

e-WHR Loans - Rs Lacs | 10 | 38 | 26 |

Farmers | 7 | 35 | 23 |

Traders | 3 | 3 | 3 |

Whrrl Platform eWHR Loans- Rs Lacs | - | - | - |

Farmers | - | - | - |

Traders | - | - | - |

Whrrl Platform eWHR Loans - No of Customers | - | - | - |

Farmers | - | - | - |

Traders | - | - | - |

Non-blockchain Banks eWHR Loans - Rs Lacs | 10 | 38 | 26 |

Farmers | 7 | 35 | 23 |

Traders | 3 | 3 | 3 |

| Exhibit 3 WHR Financing Processes for Different Types of Warehouses | |||

|---|---|---|---|

Process | Private Warehouse | Public Warehouse | |

Non-WDRA registered | WDRA registered | Non-WDRA registered | |

Stage 1 | Private warehouses designated agents to bring the customer and their goods at the warehouse. | The farmer manually searched for availability of warehouse spaces nearby and took his produce there. | |

Stage 2 | Warehouses used private ERP systems to generate receipts. These receipts were manually emailed to the banks | Warehouses used NERL systems to generate receipts. These receipts were automatically available for the banks connected via the same platform | Warehouse used ERP software/manual to generate receipts. |

Stage 3 | The depositor owner took the loan application to the banks manually. | ||

Stage 4 | Banks conducted the verification checks about the borrower’s identity and the deposit with the help of verification agencies (VA). Their activities included verification of the goods and submission of verification reports to the bank. In case the warehouse was also the Collateral Management Agency (CMA), verification of goods was done at the time of deposit itself. Warehouse emails receipt and other financial/nonfinancial to the banks. (In some cases, software such as ECBF were used to generate electronic storage receipts). | Bank checks for availability of receipts on NERL platform. It would then get the identity of the depositor verified (manual or KYC). The WDRA inspector visited the warehouse and inspected the goods (unscheduled), then uploaded verification reports on WDRA platform | Banks conducted the verification checks about the borrower’s identity and the deposit with the help of third-party agencies/internal teams. Verification Agency visited the warehouse and inspected the goods, sent verification report to the bank. |

Stage 5 | Loan was disbursed to the depositor’s account. | Loan was disbursed to the depositor’s account. Loan information was updated on the common NERL platform. | Loan was disbursed to the depositors account. |

Stage 6 | Farmer repaid the loan prior to the sale of his deposited produce. | ||

Stage 7 | Goods sold online at e-NAM platform by depositor or through NERL platform by bank (in case of default). | ||

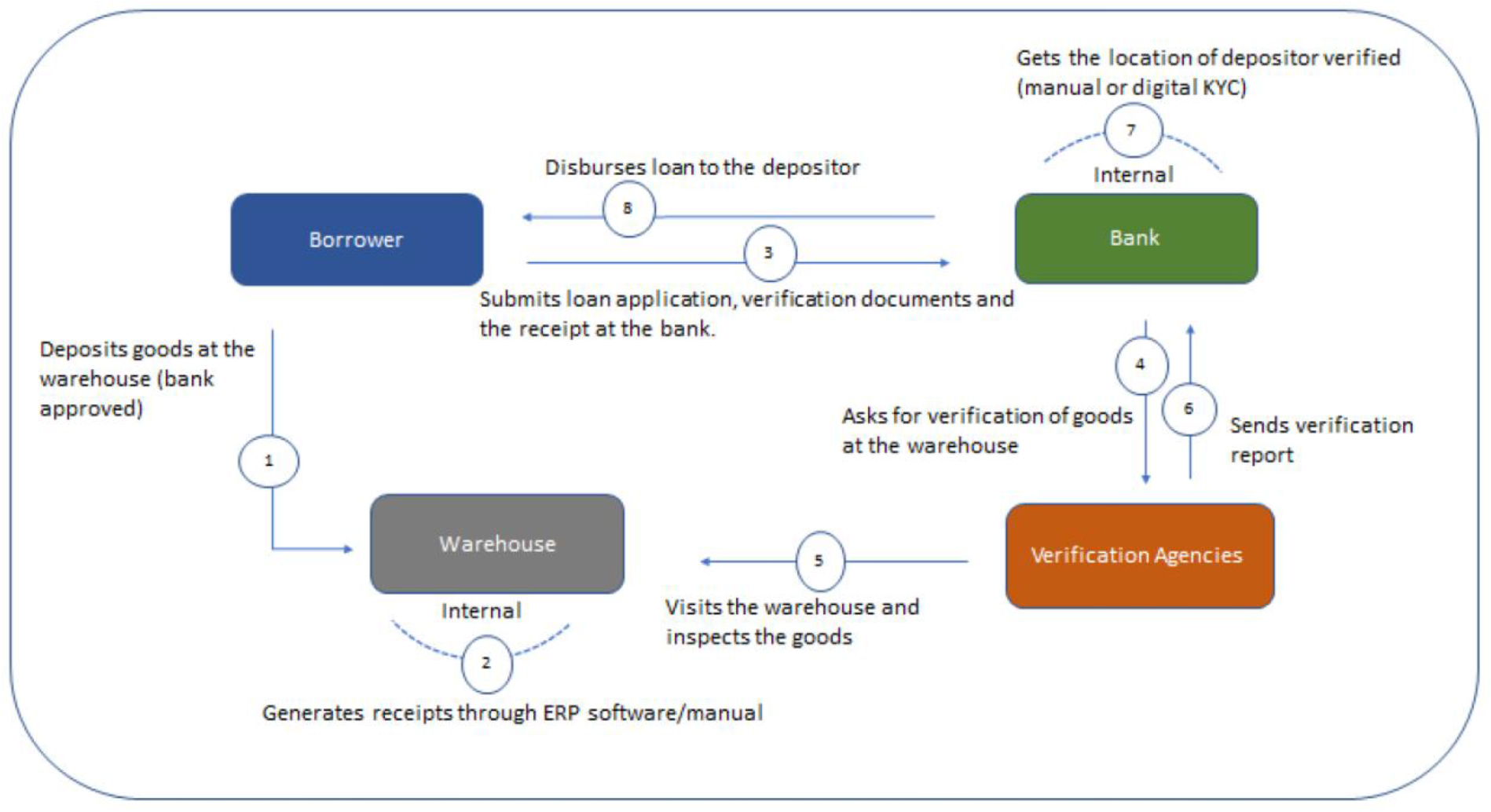

The eight steps are as follows:

The borrower deposits goods at the warehouse (bank approved).

In the warehouse, internal, generates receipts through ERP software or manual.

The borrower submits loan application, verification documents and the receipt at the bank.

The Bank asks for verification of goods at the warehouse from the verification agencies.

The verification agencies visit the warehouse and inspect the goods at the warehouse.

The verification agencies send the verification report to the bank.

Internally at the bank gets the location of depositor verified (manual or digital KYC).

The bank disburses loan to the depositor.

Exhibit 4. WHR Financing for Non-WDRA Public Warehouse

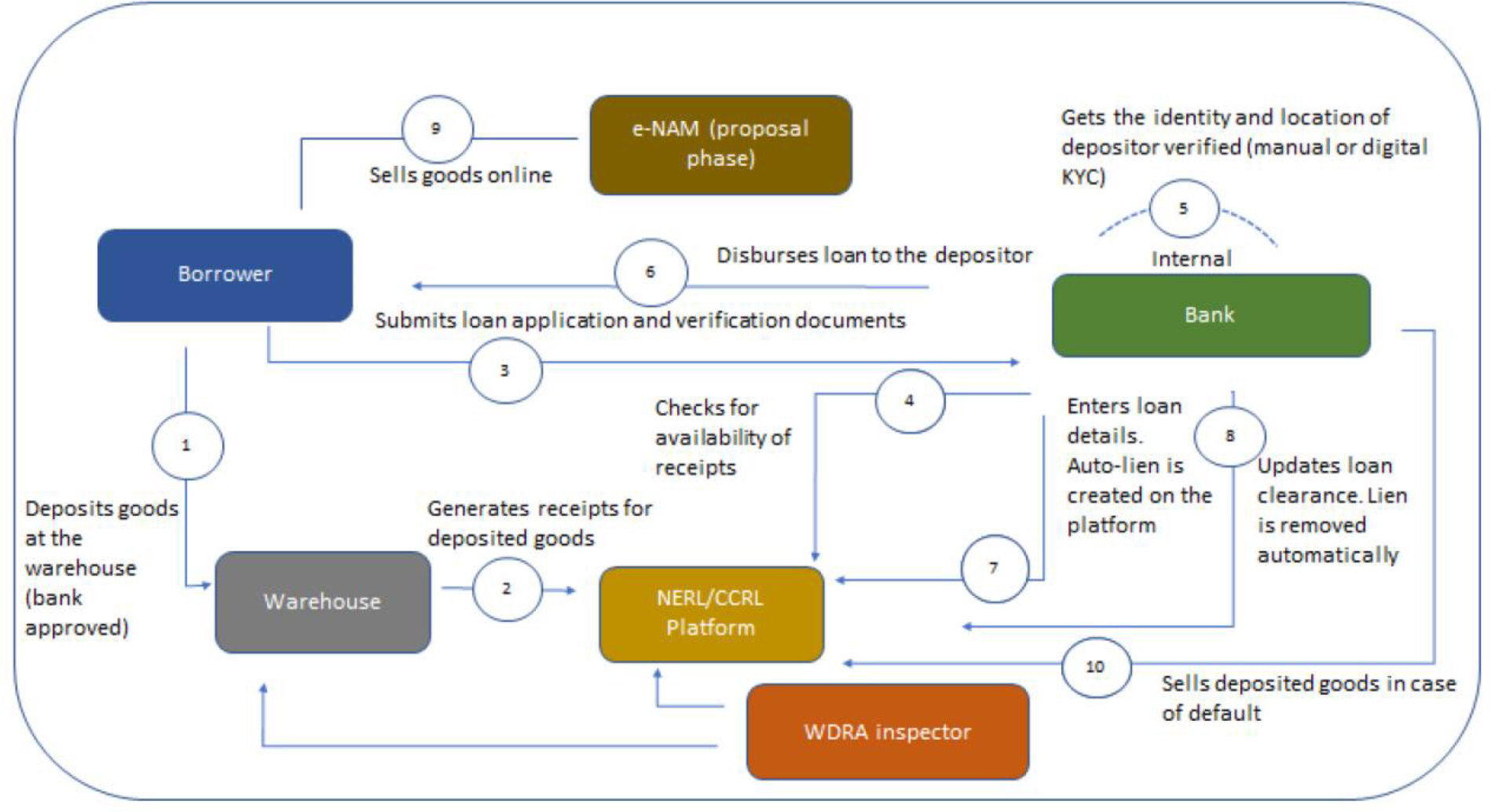

The ten steps are as follows:

The borrower deposits its goods at the warehouse (bank approved).

The warehouse generates receipts for deposited goods at the NERL or CCRL platform.

WDRA inspector checks NERL or CCRL platform and the warehouse.

The borrower submits the loan application and verification documents to the bank.

The bank checks for the availability of receipts.

Internally the bank gets the identity and location of the depositor verified (manual or digital KYC).

The bank disburses the loan to the depositor, or borrower.

The bank enters loan details. Auto-lien is created on the platform.

The bank updates loan clearance. Lien is removed automatically.

The borrower sells goods online at e-NAM (proposal phase).

The bank sells deposited goods in case of default.

Exhibit 5. WHR Financing for NERL/WDRA Registered Public Warehouse

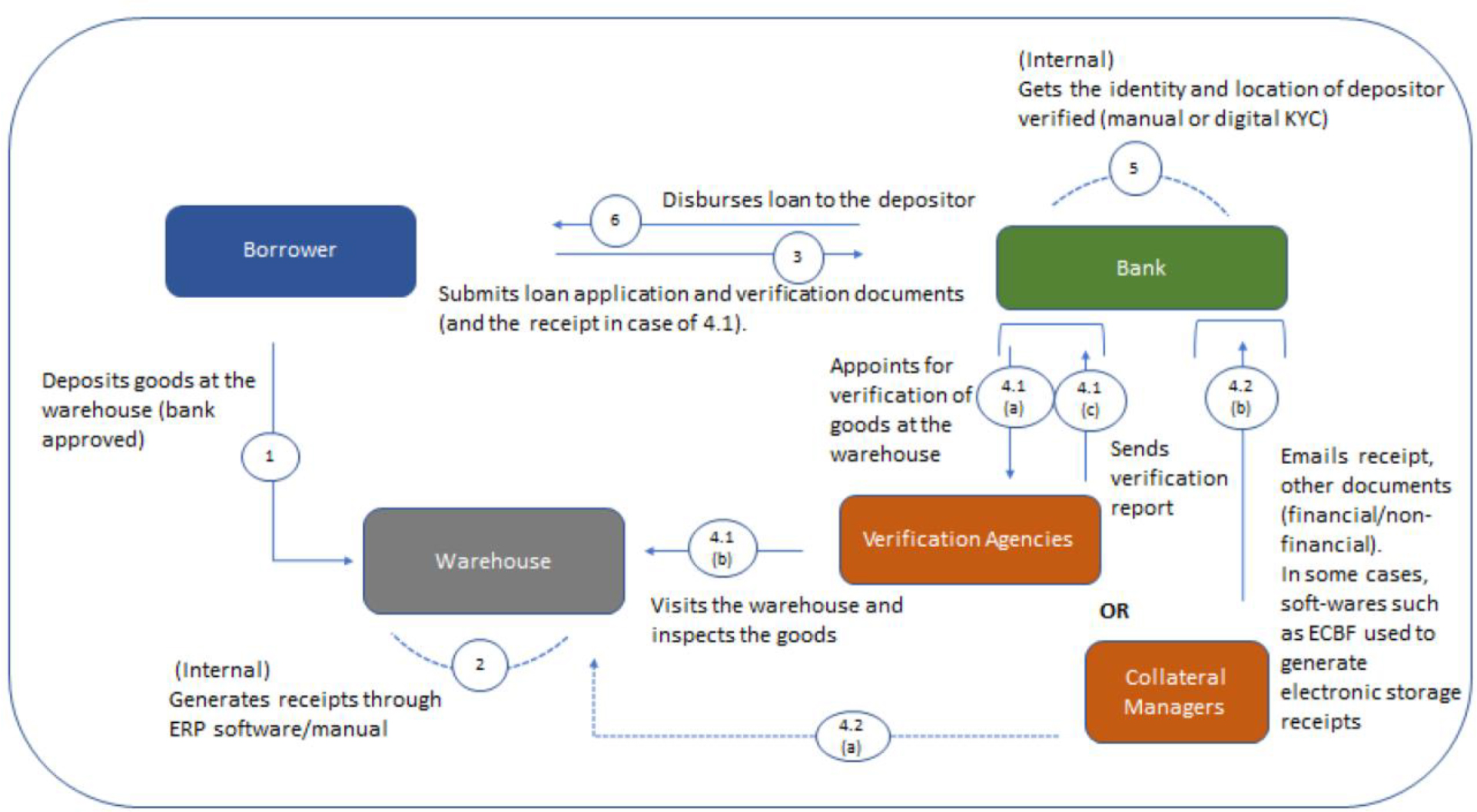

The steps are as follows:

The borrower deposits goods at the warehouse (bank-approved).

Internally the warehouse generates receipts through ERP software or manual.

The borrower submits loan application and verification documents and the receipt in case of the next step.

The bank appoints verification of goods at the warehouse.

The verification agencies visit the warehouse and inspect the goods.

The verification agencies send verification reports.

The collateral managers visit the warehouse.

The collateral managers email receipts, and other documents (financial or non-financial). In some cases, software such as ECBF is used to generate electronic storage receipts.

Verification agencies or collateral managers.

Internally the bank gets the identity and location of the depositor verified (manual or digital KYC).

The bank disburses the loan to the depositor or borrower.

Exhibit 6. WHR Financing for Non-WDRA Private Warehouse

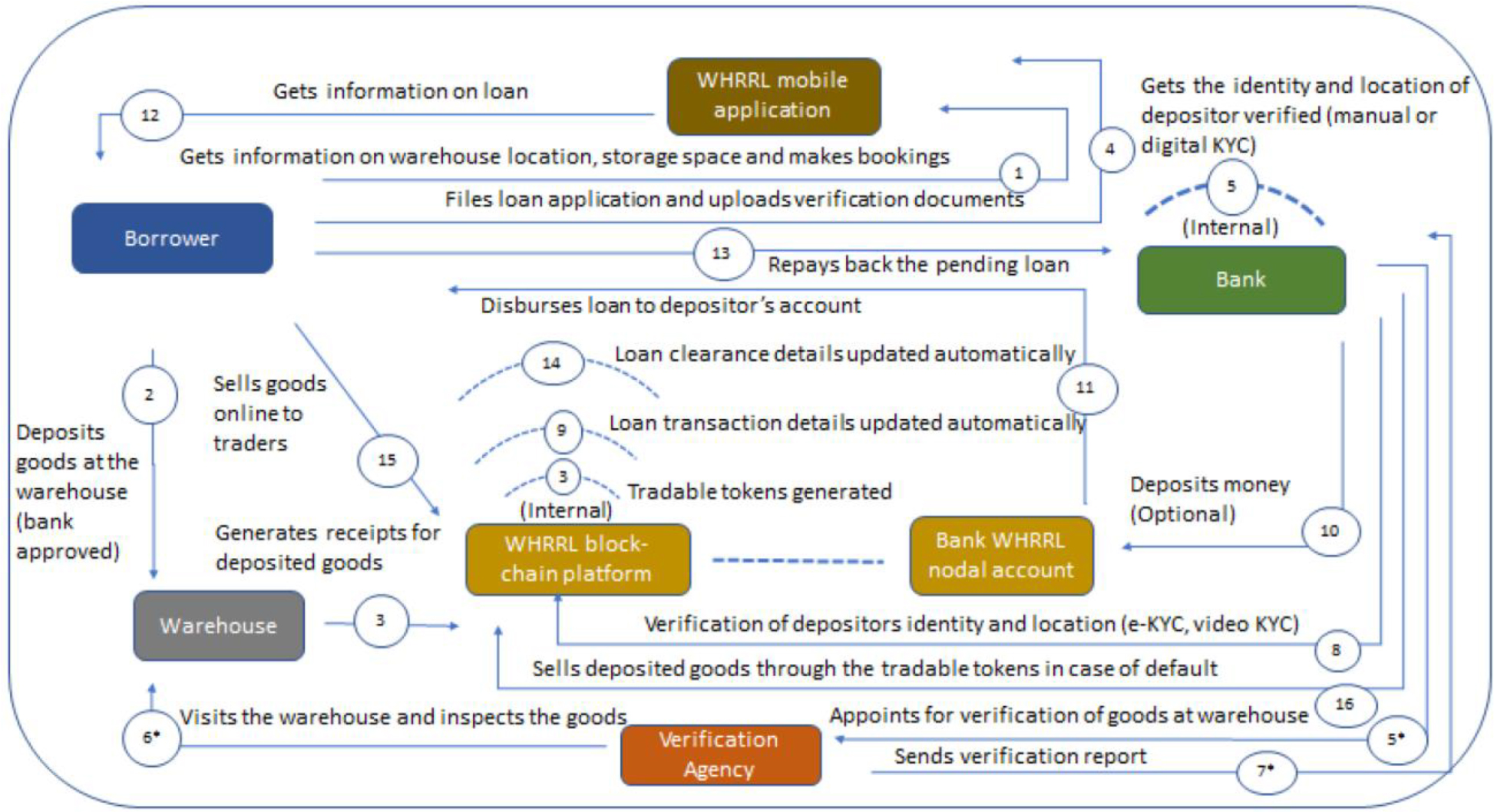

The steps are as follows:

The borrower gets information on warehouse location, and storage space and make a booking in WHRRL mobile application.

The borrower deposits goods at the warehouse (bank-approved).

Internally in Whrrl block-chain platform, the tradable tokens are generated.

The warehouse sells deposited goods through the tradable tokens in case of default.

The borrower files a loan application and uploads verification of documents via Whrrl mobile application.

Internally, the bank gets the identity and location of the depositor verified (manual or digital KYC).

The bank appoints verification agency for verification of goods at warehouse.

The verification agency visits the warehouse and inspects the goods.

The verification agency sends a verification report to the bank.

The bank, verification of depositors’ identity and location (e-KYC, video KYC) to the Whrrl blockchain platform.

Internally in Whrrl blockchain platform, loan transaction details are updated automatically.

The bank deposits money (optional) at the Bank Whrrl nodal account.

From the bank Whrrl nodal account, it disburses loan to depositor’s account, the borrower.

From the Whrrl mobile application, the borrower gets information about the loan.

The borrower repays the pending loan to the bank.

Internally in Whrrl blockchain platform, loan clearance details updated automatically.

The borrower sells goods online to traders via Whrrl blockchain platform.

The bank sells deposited goods through the tradable tokens in case of default.

Exhibit 7. WHR Financing for Whrrl-Registered Warehouse

| Exhibit 8 Whrrl’s Transactions Post the Pandemic | ||||

|---|---|---|---|---|

Apr | May | Jun | July | |

States | 1 | 1 | 1 | 1 |

No. of Locations | 5 | 195 | 193 | 193 |

No. of Warehouses | 16 | 1250 | 1250 | 1250 |

No. of Banks | 2 | 3 | 3 | 3 |

eWHR Generated (Rs. Cr.) | 14 | 661 | 1644 | 653 |

Govt | 12 | 622 | 1578 | 629 |

Farmers | 1 | 12 | 11 | 4 |

Agri Traders | 0 | 12 | 26 | 12 |

Co-operative Societies | - | - | - | 0 |

Other Entities | 0 | 16 | 29 | 8 |

Quantity (MT) | 2317 | 98,688 | 2,38,613 | 86,066 |

Govt. | 2013 | 92,810 | 2,28,206 | 81,734 |

Farmers | 206 | 1870 | 2398 | 1051 |

Agri Traders | 80 | 3147 | 6330 | 2669 |

Co-operative Societies | - | - | - | 72 |

Other Entities | 18 | 861 | 1680 | 541 |

e-WHR Loans - Rs Lacs | 14 | 148 | 257 | 576 |

Farmers | 4 | 77 | 88 | 100 |

Traders | 11 | 72 | 169 | 475 |

Whrrl Platform eWHR Loans - Rs Lacs | - | 10 | 4 | 450 |

Farmers | - | 10 | 4 | 50 |

Traders | - | - | - | 400 |

Whrrl Platform eWHR Loans - No of Customers | - | 4 | 2 | 20 |

Farmers | - | 4 | 2 | 18 |

Traders | - | - | - | 2 |

Offline Banks eWHR Loans - Rs Lacs | 14 | 138 | 253 | 126 |

Farmers | 4 | 67 | 84 | 51 |

Traders | 11 | 72 | 169 | 75 |

Notes

1Blockchain is a transaction database shared by all nodes participating in the system. It makes the history of a transaction unalterable and transparent through the use of cryptographic hashing and decentralization respectively. This allows people to share valuable data in a secure manner and thus reduced risks and frauds and brought transparency at a scale.

2The name ‘Whrrl’ refers to warehouse receipt loans.

3Blockchain Advisory Council (BAC) was co-founded by Ashish in 2018 as an advisory and consulting firm specialising in digital, crypto, decentralised, blockchain and information technologies.

4In 2014, at Qingdao port in China, fraudulent receipts were issued several times against metals held in warehouses as collateral for loans. This resulted in storage scams worth $648 million.

5Bharti, N. (2018). Evolution of agriculture finance in India: a historical perspective. Agricultural Finance Review, 78(3), pp. 376–392

6Ibid.

7Ibid.

8Subbarao, D. (2012, July 12). Agricultural credit – Accomplishments and Challenges. Reserve Bank of India. Retrieved from https://rbidocs.rbi.org.in/rdocs/Speeches/PDFs/ACACHA120712.pdf

9Ibid.

10Ibid.

11Vighneswara, S. (2016). Analyzing the agricultural value chain financing: approaches and tools in India. Agricultural Finance Review, 76(2).

12 Panda, B. & Joy S. (2019). Dynamics of Technological Evolution in Indian Banking. Retrieved from https://www.nibmindia.org/admin/fckImages/B%20Panda%20319-343(1).pdf

13Grant Thornton (2017). Financial Inclusion in Rural India, Banking and ATM sector in India. Retrieved from https://www.grantthornton.in/insights/articles/financial-inclusion-in-rural-india/

14Vighneswara, S. (2016). Analyzing the agricultural value chain financing: Approaches and tools in India. Agricultural Finance Review, 76(2).

15Ibid

16See note 8 above.

17Bhatt, V. V., & Mundial, B. (1989). Financial innovation and credit market development (No. 52). Washington DC: World Bank.

18Jairath, M. S., Haque, E., & Anu, P. V. (2016). Issues Limiting the Progress in Negotiable Warehouse Receipt (NWR) Financing in India. Agricultural Economics Research Review, 29, 53–59.

19National Institute of Public Finance and Policy (2015). Report on warehousing in India Study commissioned by the Warehousing Development and Regulatory Authority. Retrieved from https://wdra.gov.in/documents/32110/38476/Report12.pdf/fcfa2f56-a673-a5f6-a870-f73292eab04a

20See note 18 above.

21See note 19 above.

22BusinessWire (2020, May 21). The Warehousing Market in India 2020; Expected to be Worth INR 2,821 Billion by 2024 - ResearchAndMarkets.com. Retrieved from https://www.businesswire.com/news/home/20200521005412/en/The-Warehousing-Market-in-India-2020-Expected-to-be-Worth-INR-2821-Billion-by-2024---ResearchAndMarkets.com

23See note 19 above.

24Hussain, S. (2018, September 25). Warehousing receipt system: the missing link. Live Mint. Retrieved from https://www.livemint.com/Opinion/yFKdPGvwK5IHsKtSChpmwJ/Opinion--Warehousing-receipt-system-the-missing-link.html

25Dey, K., & Alur, S. (2016). Warehouse to Manage Collateral—Kaul’s Dilemma. Asian Case Research Journal, 20(01), 133–175.

26See note 19 above.

27Note - Within the diverse agricultural commodities, Whrrl focuses largely on grains, pulses and cash crops that can be stored in ambient warehousing, as banks are hesitant about lending against perishable commodities.

28See note 24 above.

29Burton, M. (2017, January 2017). Forged Warehouse Receipts Renew Worries of Commodities Fraud. BloombergQuint. Retrieved from https://www.bloombergquint.com/markets/forged-warehouse-receipts-renew-concerns-over-commodities-fraud

30 Assalve, D. & Ma, E. (2017, December 06).WAREHOUSING: The biggest warehouse frauds of recent times. Fastmarkets Metal bulletin. Retrieved from https://www.metalbulletin.com/Article/3768844/WAREHOUSING-The-biggest-warehouse-frauds-of-recent-times.html

31See note 29 above.

32Fuzamei (2018, September 04). How Blockchain Can Prevent Warehouse Receipt Financing Fraud. The Medium. Retrieved from https://medium.com/@fuzameitwitter/how-blockchain-can-prevent-warehouse-receipt-financing-fraud-32933d89a0b3

33See note 30 above.

34Ibid.

35Alexander, G.S. (2007, January 19). ICICI takes Rs 150-cr hit on farm loan fraud. The Economic Times. Retrieved from https://m.economictimes.com/industry/banking/finance/banking/icici-takes-rs-150-cr-hit-on-farm-loan-fraud/articleshow/1289166.cms

36Shenoy, D. (2013, September 23). NSEL: The 5,500-crore Scam No One Wants to Deal With. Retrieved from https://www.capitalmind.in/2013/09/nsel-the-5500-crore-scam-no-one-wants-to-deal-with/IANS (2014, May 7). Jignesh Shah, another arrested in NSEL scam. Retrieved from https://www.business-standard.com/article/news-ians/jignesh-shah-another-arrested-in-nsel-scam-114050701532_1.html

37Rao, M.T. (2019, December 13). Traders Defrauded several banks of Rs 400 crores in Andhra Pradesh. United News of India. Retrieved from http://www.uniindia.com/traders-defrauded-several-banks-of-rs-400-cr-in-andhra-pradesh/south/news/1820699.html

38Voshmgir, S. (2019). Block chain hub Berlin. Retrieved from http://blockchainhub.net/smart-contracts/

39Bhardwaj, C. (2020, January 9). What is Zero-Knowledge Proof & its Role in the Blockchain World? Retrieved from https://appinventiv.com/blog/zero-knowledge-proof-blockchain/

40World Health Organisation (2020, July 31). Coronavirus disease (COVID-19) Situation Report–193. Retrieved from https://www.who.int/docs/default-source/coronaviruse/situation-reports/20200731-covid-19-sitrep-193.pdf?sfvrsn=42a0221d_4

41Jones, L. et al. (2020, June 30). Coronavirus: A visual guide to the economic impact. BBC. Retrieved from https://www.bbc.com/news/business-51706225

42See note 40 above.

43Jagannath, J. (2020, May 29). Covid-19 impact: India GDP growth slows to 3.1% in March quarter. Live Mint. Retrieved from https://www.livemint.com/news/india/covid-19-impact-india-gdp-growth-at-3-1-in-q4fy20-11590751970512.html

44Gruenwald, P. (2020, July 1). Economic Research: The Global Economy Begins A Slow Mend As COVID-19 Eases Unevenly. S & P Global Ratings.

45Based on field data, as per internal market research by Whrrl.

This case study is provided in this Sage Business collection primarily as a basis for classroom discussion or self-study and is not meant to illustrate either effective or ineffective management styles. Nothing herein shall be deemed to be an endorsement of any kind. This case study is for scholarly, educational, or personal use only within your university, and cannot be forwarded outside the university or used for other commercial purposes.

© 2026 Sage Publications, Inc. All Rights Reserved.

Get a 30 day FREE TRIAL

-

Watch videos from a variety of sources bringing classroom topics to life

Watch videos from a variety of sources bringing classroom topics to life -

Read modern, diverse business cases

-

Explore hundreds of books and reference titles

Read next

More like this

Sage Recommends

We found other relevant content for you on other Sage platforms.

Have you created a personal profile? Login or create a profile so that you can save clips, playlists and searches