Summary

Contents

Subject index

Product and Services Management provides a holistic approach to the study of product and services management. Authors George Avlonitis and Paulina Papastathopoulou look at the key milestones within a product’s or service life cycle and considers in detail three crucial areas within product management, namely product/service portfolio evaluation, new product/service development and product/service elimination. Based on research conducted in Europe and North America, this book includes revealing cases studies that will help students make important connections between theory and practice.

Appendix 1: New Product Budget1

The present appendix describes the theoretical background regarding the process of developing a budget for a new product. A real-life example is also provided.

Theoretical Background

The time period covered by a new product budget is usually twelve months, or an accounting period, depending on the policy followed by the company. In addition, this budget can be developed into a monthly, quarterly, semi-annual or other frequency that is considered to be appropriate by the company. The time period on which the budget analysis will be based depends on the existing control procedures regarding its implementation, namely, the comparison of the budgeted with the actual figures in order to calculate the variances, justify them and make the right decisions and necessary corrective actions.

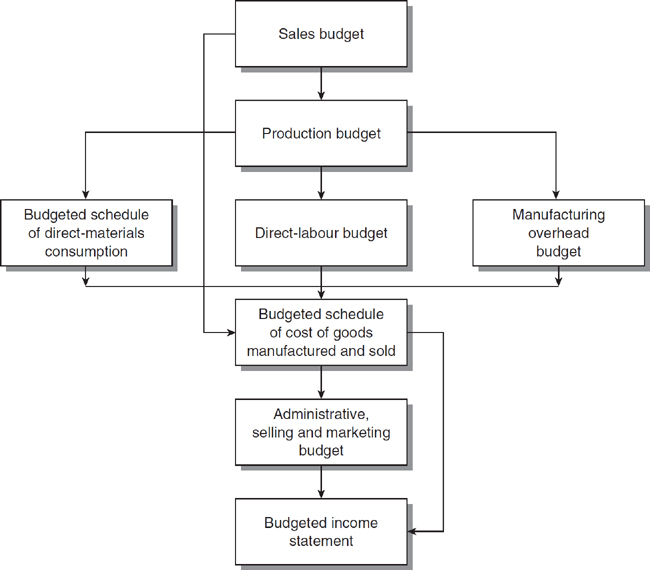

The development of a new product budget is called master budget. A number of separate budgets compose the master budget of the new product (Figure 1). These budgets are developed either sequentially or in parallel.

Figure 1 New product budget development

The basic elements of the separate budgets are briefly presented below.

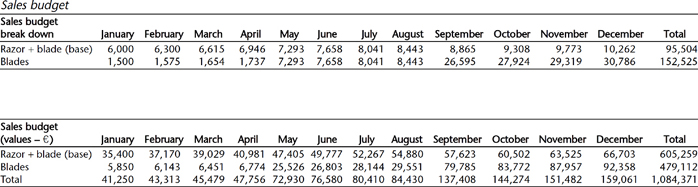

Sales Budget

The sales budget forms the basis of the master budget. In this sense, the accuracy of the sales budget is extremely important for developing the master budget. Specifically, an over-estimation of demand may lead to the creation of undesired inventories and an unnecessary commitment of resources, which could possibly be used more efficiently in other company products. On the other hand, an under-estimation of demand may not allow the company to satisfy its customers' needs and, thus, lose profits and market share.

Sales forecasting can be done in different ways depending on the policy that each company follows. The basic methods of sales forecasting are as follows: subjective/qualitative methods, for example, estimations of sales directors and sales persons, analysis of customers' intentions and objective/quantitative, for example, market testing. In either method, a series of internal and external factors must be taken into account. The main internal factors are: sales of previous versions of the product or similar products of the previous year, production capability of the company, marketing and sales promotion strategies, product seasonality, expected life cycle of the product, and so on. The main external factors that may be considered are: competitive and substitute products, economic conditions and negotiating power of company's customers, general economic conditions, general trends in the manufacturing industry and governmental policies.

In order to develop the sales budget, the pricing policy for the new product must also be considered. Thus, decisions about the sales price, the discount policy, the special offers of the product, are important parameters in developing the sales budget. Sales are budgeted as follows:

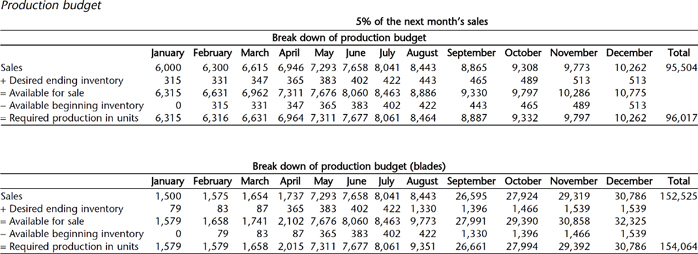

Production Budget

The production budget is based on the sales budget after making the necessary adjustments in the level of the desired ending inventories of finished goods. Specifically, by taking into account: the inventory of finished goods at the beginning of the month, the expected sales during the month, and the desired inventory at the end of the month, the quantities that must be produced on a monthly basis can then be calculated. The level of inventories retained is relevant to the policy followed by the company and is affected, among others, by the vulnerability of the product, the speed of its technological obsolescence and the warehousing costs. Production can be budgeted as follows:

Based on the production budget, a company can develop the budgets for direct materials, direct labour and manufacturing overheads, as is presented further down in this chapter.

Budgeted Schedule of Direct-Materials Consumption

Direct materials are all the raw materials that are incorporated into the product and they constitute an important part of the total cost of the materials that will be consumed for its production. Direct materials are part of the direct cost because they are directly associated with the product.

The scheduled budget of direct material consumption is referred to the quantity and the cost of direct materials that are necessary for producing the required product units according to the production budget. The direct materials consumption is budgeted as follows:

Direct Labour Budget

Direct labour is the labour offered by those who are directly involved in the processing of direct materials that are incorporated into the product, and it constitutes an important part of the cost of the total labour that will be required for its production. Direct labour is part of the direct cost because it is directly associated with the product. Direct labour may be required during the whole range of processing activities that take place from the original shaping to the final production of the product. Finally, the cost per direct labour hour in each department, namely, the hourly labour cost per department varies according to the remuneration policy of the company. Hence, direct labour is budgeted as follows:

Manufacturing Overhead Budget

Manufacturing overheads are the indirect costs that are incurred in the context of a production process of a company and must be allocated to all of the products produced. Examples of such expenditure are: indirect or other materials, indirect labour, various operational expenses (rent, energy, insurance, depreciation, utilities), and so on. The calculation of manufacturing overheads that should be allocated to the new product should incorporate not only the manufacturing overheads that are directly associated with the new product, but also the manufacturing overheads that concern the total production of the new product (or part of it). It should be noted that manufacturing overheads that should be associated with the new product will be calculated by multiplying an allocation rate of manufacturing overheads determined by the company with the base used for the allocation (for example direct labour hours, number of machine hours, number of product units, and so on). Thus, manufacturing overheads can be budgeted as follows:

On the basis of the information provided from the budgets of direct-material consumption, direct labour and manufacturing overheads, the budgeted production cost per unit can then be calculated.

Budgeted Schedule of Cost of Goods Manufactured and Sold

The cost of goods manufactured during a period involves the cost of the products that were finished during this period and it is calculated as the sum of direct materials consumed, direct labour and manufacturing overheads.

The cost of goods sold during a time period refers to the cost of the products that were sold during this period and it is the sum of the value of the beginning inventory of finished goods and the cost of manufactured goods minus the value of ending inventory of finished products. The valuation of inventories is based on the method used by the company namely LIFO (last in, first out), FIFO (first in, first out) or weighed average method.2

Administrative Expense Budget

The general administrative expenses are the expenses created in the general context of a company's administration. Examples of such expenses are the expenses of supporting departments such as the accounting department, the human resource management department, the legal services, but also the General Manager's salary, rent, electricity and so on. In most cases there are no direct administrative expenses related to a new product. Usually the budgeted administration expenses that are associated with the new product are calculated by multiplying the budgeted sales value of the new product with a predetermined rate.

Selling and Marketing Expenses Budget

The selling and marketing expenses are the expenses created in order to promote sales and deliver the products to the customer. Examples of such expenses are advertising costs, the salaries of the Sales and Marketing Managers, the salaries and commissions of sales staff, the expenses of participating in trade shows, the storage expenses of finished products, the transportation expenses of finished products, the market research expenses, the promotion expenses, and so on.

The budgeted selling and marketing expenses of the new product are direct and indirect. The direct selling and marketing expenses of the new product concern the special promotion activities for the new product (free samples, advertisements), listing fees, and so on, and, therefore should be allocated only to this product. The indirect selling and marketing expenses refer to the expenses that are associated with the new product, for example the proportion of sales staff salaries and those of their managers, their travelling expenses, the cost of participating in exhibitions, and so on. However, a portion of them should be allocated to the new product as well. The budgeted selling and marketing expenses that are associated with the new product are calculated by multiplying the budgeted sales value of the new product with a predetermined rate.

Budgeted Income Statement

The budgeted income statement is based on the previous budgets. This statement presents the budgeted gross income (profit or loss) of the new product as well as the operating income (profit or loss) of the new product.

Sensitivity Analysis and Scenario Planning

Given the complexities and uncertainties of the business world, unexpected changes usually occur. In this sense, companies need to examine their forecasts and assumptions on a regular basis. To do this, sensitivity analysis and scenario planning are often performed.

In sensitivity analysis one or more parameters that participate in the budget development are changed. The parameters that are proved to have a considerable impact on the profitability and the viability of the new product are identified and carefully monitored.

In scenario planning, companies prepare different combinations of a number of parameters. Usually, companies determine the pessimistic, the normal and the optimistic scenario and estimate their outcomes by assessing both the financial and the non-financial results from the introduction of the new product in the market.

A Real-Life Example of a New Product Budget

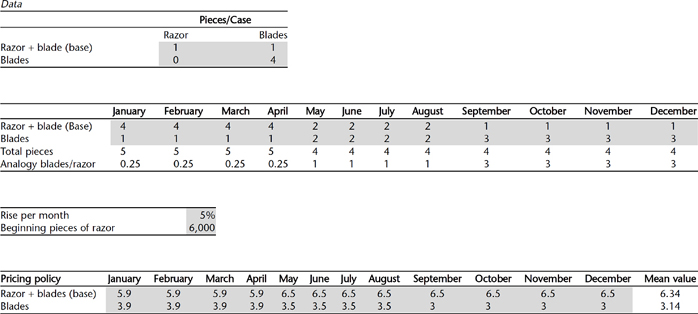

The new product development department of Razors' Manufacture S.A.3 is currently assessing the possibility of launching a new modern razor for women into the market. This razor, which will guarantee soft skin, will have an anatomic shape and will be available in pleasant colours. In addition, it will be sold with a modern case, which will make the product a nice bath accessory. The product will be introduced to the market in two variants. The first one will be the razor device with the blade (henceforward razor), while the second one will be the shaving cartridge consisting of four blades (henceforward blades).

Financial Data of the Product

- The expected sales mixture and pricing policy for the first year of the product's introduction to the market organized in quartiles have been determined as follows:

- The expected demand, based on a marketing research that has been previously conducted and costed at €44,645, showed that 6,000 razors, with conservative estimates, could be sold during the first month of introduction with a monthly rise of 5 per cent.

- The company has as a policy of producing each month only as many product units as to cover the monthly demand plus 5 per cent of the expected sales of the next month.

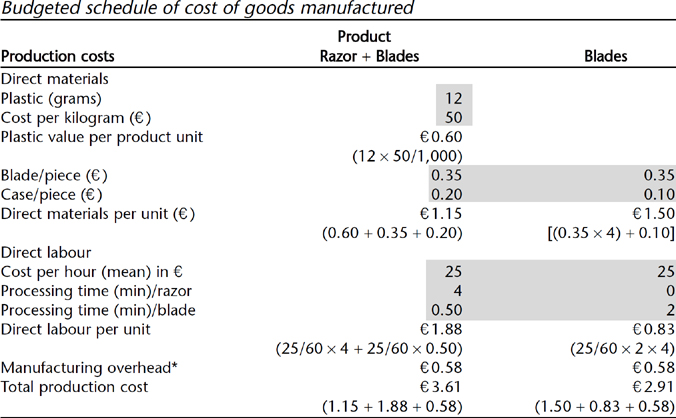

- The technical descriptions of the products regarding direct materials and direct labour, are presented below:

Cost data Razor Blades Direct materials Plastic (grams) 12 Cost per kilogram (€) 50 Blade/piece (€) 0.35 0.35 Case/piece (€) 0.2 0.1 Direct labour Cost/hour (mean value in €) 25 25 Processing time for the razor (min) 4 0 Processing time for the blade (min) 0.5 2 The company allocates manufacturing overheads using as an allocation base the expected number of the products to be produced on a yearly basis.

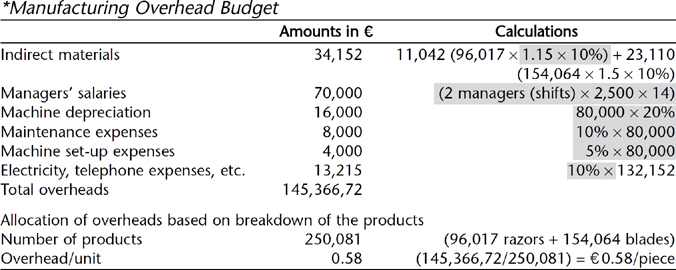

- The annual manufacturing overheads regarding the two products are:

Manufacturing overhead budget Indirect materials 10% of direct materials' value Managers' salaries Two managers, one for each shift with a total monthly cost of €2,500 Machine depreciation For the production of the new products a new machine will be bought. Its value will be €80,000 and its useful life 5 years (depreciation rate 20%). The machine will be paid in 5 monthly equal instalments Maintenance expenses Expected to be 10% of the machine's acquisition cost value (annually) Machine set-up expenses Expected to be 5% of the machine's acquisition cost value (annually) Electricity, telephone expenses, etc. Expected to be 10% of other overheads - The annual selling and marketing expenses regarding the two products have been budgeted as follows:

Budgeted selling and marketing expenses Advertising 1% of the monthly sales value Sales persons' salaries Five sales persons will spend 5% of their time in the promotion of the product. Each of them will have a monthly salary of €2,000. Sales persons' commissions The sales persons will receive 0.05% of the sales as a commission. Distribution expenses Have been budgeted to be €0.10 per item of product. Market research It was decided to allocate the cost of market research in each product unit based on the budgeted sales of the first year. Listing fees The listing fees have been estimated to be €3,000. - The administration expenses are expected to mount to 8 per cent of the sales value.

Based on the above data, the following budgets for the first year of the new product introduction can be developed both on a monthly and a yearly basis:

- sales budget in units of each product;

- sales budget in values;

- production budget in units of each product;

- budgeted schedule of cost of goods manufactured per product unit;

- budgeted schedule of selling, marketing and administration expenses;

- budgeted income statements.

It is noted that, in the following exhibits the grey parts refer to the basic assumptions that have been made during the budget development of the new product, while the white parts provide the results of the computations based on these assumptions. In changing these assumptions, the results will change as well. The analysis that follows can be undertaken using any spreadsheet software package.

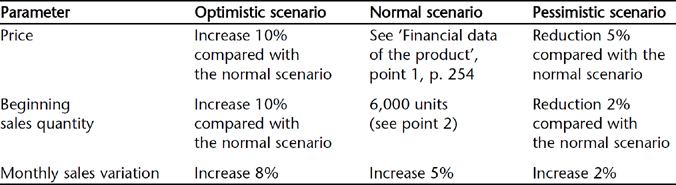

Finally, in order to assess whether the new product is efficient in financial terms under alternative conditions, the company prepared three scenarios: the optimistic, the normal, and the pessimistic making different assumptions regarding the sales price of the products, the number of units sold with which the budget will begin and the rate of sales variation.

These assumptions are the following:

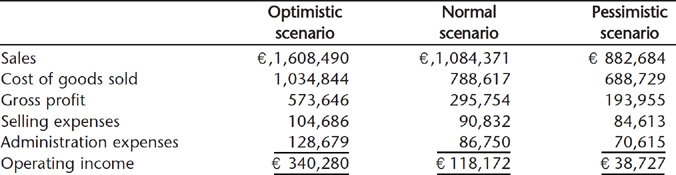

The results of the three scenarios in terms of operating income are the following:

From the above analysis, it is obvious that in case the pessimistic scenario is verified, the sales as well as the profitability of the new product will certainly be lower in comparison to the figures of the normal scenario by 18.63 per cent and 67.23 per cent, respectively. On the other hand, in case the optimistic scenario comes true then sales and operating income will be increased by 48.33 per cent and 187.95 per cent respectively in relation to the normal scenario. It has to be noted, though, that under any scenario the new product seems to be a profit-making project.

Notes

1 This appendix was prepared by Dr Sandra Cohen, Lecturer in Accounting at the Athens University of Economics and Business, under the guidance of Professor George J. Avlonitis.

2 For a discussion on these methods, see any basic accounting textbook.

3 The name of the company is disguised for confidentiality reasons.

Further Reading

- Loading...

Get a 30 day FREE TRIAL

-

Watch videos from a variety of sources bringing classroom topics to life

Watch videos from a variety of sources bringing classroom topics to life -

Read modern, diverse business cases

-

Explore hundreds of books and reference titles

Read next

More like this

Sage Recommends

We found other relevant content for you on other Sage platforms.

Have you created a personal profile? Login or create a profile so that you can save clips, playlists and searches